Back

Share

Like

trend

Article Highlights

Korean retail is defined by ambivalence, where consumers precisely mix budget purchases with premium indulgences.

Small-format indulgence categories like desserts and fragrance generate outsized revenue per square meter.

Validation followed by full-price purchase is now a structural consumer pattern in Seoul.

A recession doesn't eliminate consumer desire. It compresses it — into smaller units, higher frequency, and a much sharper sense of where the value actually is. Korean consumers in 2026 are not spending less. They are spending differently. The same person buying budget coffee on the commute is spending freely on a premium dessert at lunch. The person who won't upgrade their phone is buying Daiso skincare in bulk. Frugality and indulgence are operating simultaneously, within the same individual, on the same day. That's not contradiction — it's precision. And it has significant implications for what retail formats survive.

The Coffee Divide: Efficiency vs. Experience

For a caffeine transfusion

The low-cost coffee segment — Mega Coffee, Compose Coffee, Mammoth Coffee — has moved well beyond "cheap alternative" territory. These chains now carry top-tier celebrity endorsements, invest in brand identity, and position themselves as a rational lifestyle choice rather than a concession. Their domestic market is reaching saturation, so expansion has gone international. The model is proving scalable. High volume, thin margins, strong brand equity — it works.

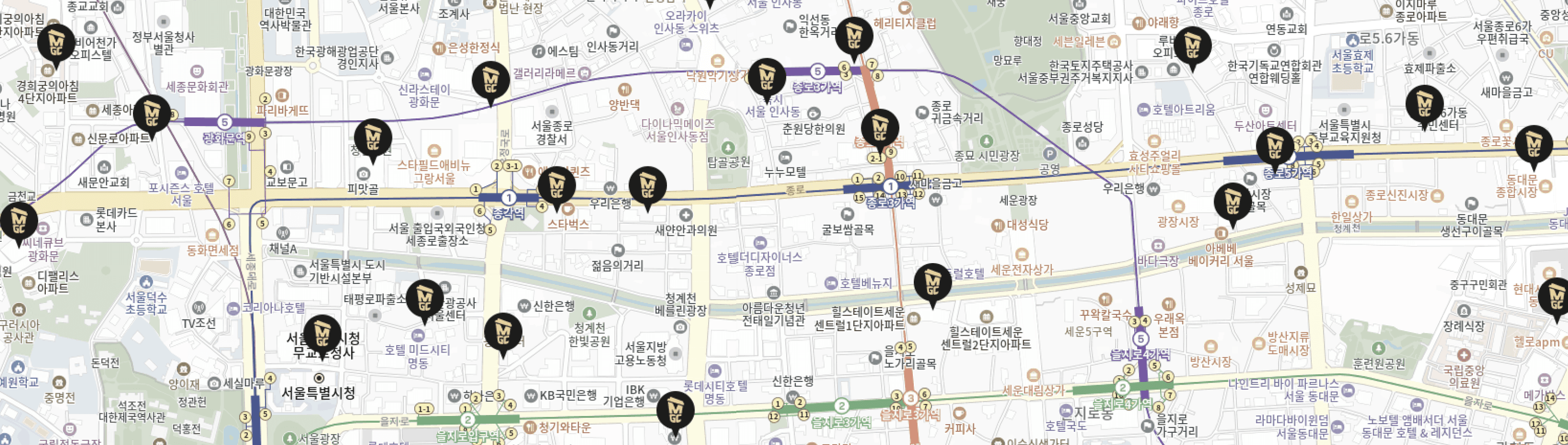

A single building facade housing four different low-cost coffee brands, symbolizing the hyper-competitive "Caffeine Transfusion" demand and overwhelming market dominance in the Jonggak Station business district.

Current distribution of Mega Coffee outlets within the Seoul CBD (Central Business District). (Source: Mega Coffee)

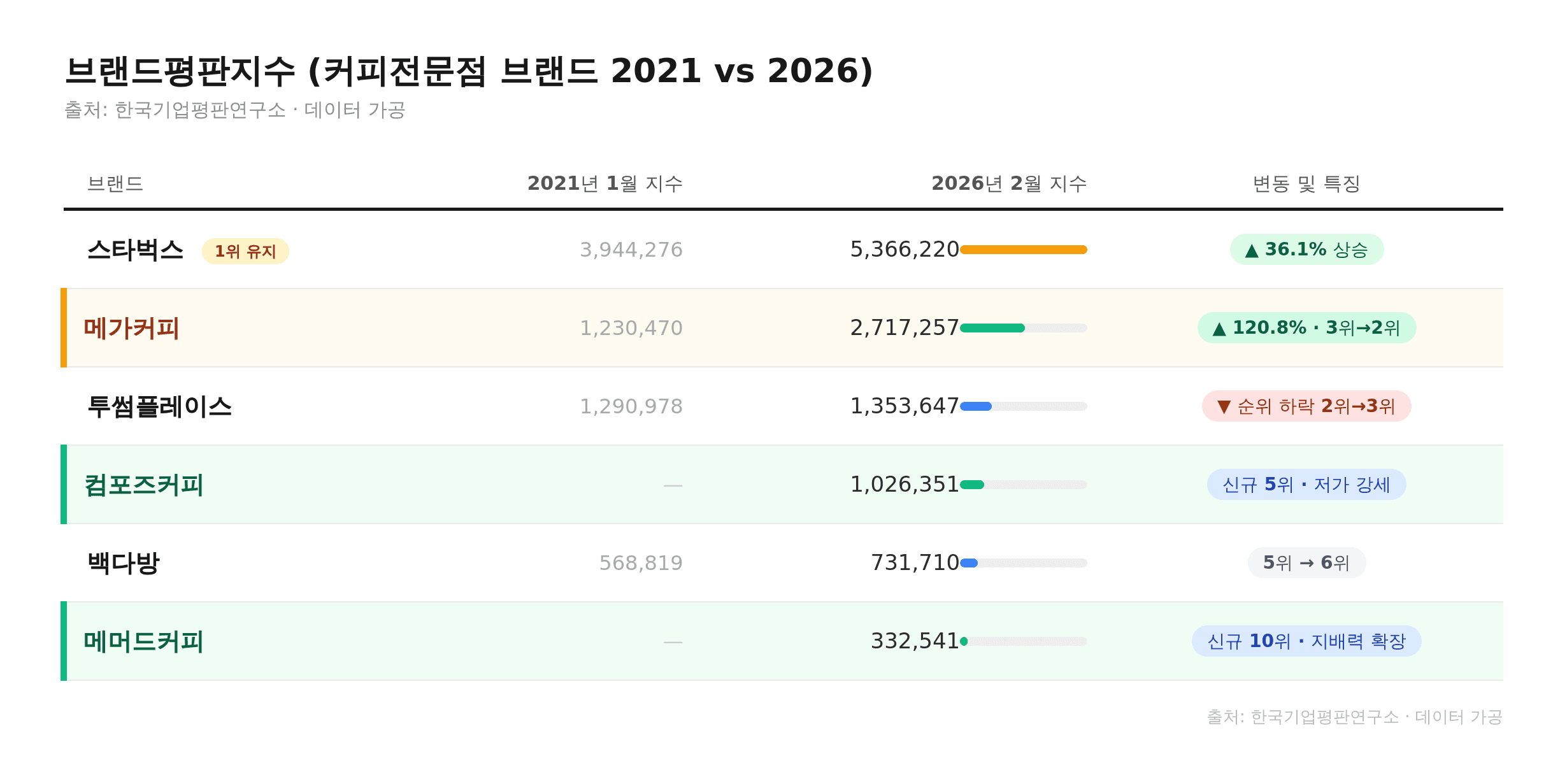

Comparing brand reputation index figures from 2021 to 2026, the growth of low-cost coffee brands is clearly visible in the data.

For immersive experience

On the opposite end, the standing espresso bar has carved out a durable niche. In dense office districts, these are five-minute resets in the middle of a compressed workday — dense flavor, minimal footprint, minimal time. The consumer who uses Mega Coffee for fuel and a standing espresso bar for a moment of quality isn't being inconsistent. They're optimizing across different needs at different times of day.

The CBD Reset: Espresso bars near Jonggak Station serve as hybrid spaces where High Turnover meets Brand Experience. These standing-only formats are the optimized retail model for office districts, offering professionals a momentary high-quality escape within a short lunch break.

Premium Sensibility at Accessible Prices

The popularization of niche fragrance and the modern lipstick effect transformed into small luxury

The niche fragrance category — once the exclusive territory of imported brands with five-figure price tags — has moved into everyday consumption. Domestic brands like NONFICTION, Tamburins, and Granhand have built genuine followings, partly because they offer access to brand identity at a fraction of the cost of the imports they reference.

A hand cream or room spray at 50,000 won lets a consumer own the mood and the associations of a premium brand without the financial exposure of a full fragrance purchase. This is the lipstick effect updated for 2026: not lipstick, but scent. Not recession-era consolation, but a deliberate trade-off between access and cost.

This pattern is visible in the foreign visitor data as well. International tourists in Bukchon and Seongsu are driving significant spending at fragrance specialty stores and Olive Young, concentrated in products under 100,000 won. Accessible luxury with high perceived identity value is exactly what that demographic is looking for.

Tamburins in Seongsu. Tamburins is a distinctive domestic brand that expanded the niche category of fragrance into mainstream consumption. In particular, by using “experimental spaces” as a device, it visualizes brand storytelling and offers visitors a synesthetic brand experience that goes beyond simply selling products.

Maybe I can’t buy Chanel, but I can at least buy a ‘Dujjonku’

High-priced desserts targeting the psychological Maginot line amid ultra-low-cost consumption

The "dujjonku" — a Dubai-style pistachio-cream cookie — sold for 7,000 to 8,000 won per piece at the height of its popularity. For context, that's the price of a full lunch in many parts of Seoul. And yet it sold out continuously, across multiple chains, for months.

The explanation isn't irrationality. It's the structure of small indulgence. Consumers are cutting expenses on categories where they don't find value — and redirecting that freed-up budget into a single, clearly justified premium experience. The coffee they saved money on became the dessert they spent freely on. The categories are connected.

From a retail standpoint, the dujjonku moment demonstrated something important: consumers will pay a premium price for a small-ticket item if the value proposition is clear and the psychological ceiling is accessible. Major chains — Starbucks, Baskin-Robbins, A Twosome Place — launched their own versions within weeks. One café near Jonggak Station reportedly nearly tripled sales after introducing it. That speed of response, and that scale of effect, is worth paying attention to.

“Dujjonku” products that maintained prices around 8,000 won until early February have begun price reductions. Despite improved price competitiveness, the open-run phenomenon seen before has not reappeared. This suggests that as trend cycles in the dessert category shorten, scarcity-based conspicuous consumption is fading and demand within commercial districts is shifting to new categories.

Aggressive menu launches and mass-production systems were established, but due to market saturation, consumer interest is gradually declining. (Source: brand websites)

Small-Scale Customization: Bolkku and the DIY Economy

An experiential retail trend centered on immersion and achievement through custom experiences

The bolkku trend — ballpoint pen customizing, concentrated in the Dongdaemun materials market — is a small thing that points to something larger. The experience of assembling something by hand, with your own choices, for a low price, delivers a sense of ownership and achievement that a finished product bought off a shelf doesn't replicate.

This pattern shows up in retail format decisions elsewhere: brands offering customizable keyrings, build-your-own stationery sets, monogramming services on accessories. The common thread is consumer participation in the outcome. In a market where consumers are cautious about discretionary spending, giving them authorship over the product changes the value calculation.

Driven by SNS virality, the rapidly growing “bolkku (ball-chain decorating)” trend is drawing huge crowds of domestic and international visitors to the Dongdaemun materials market (Source: AI-regenerated image based on Dongdaemun materials mall photos). This DIY trend has expanded into general retail shops as well, where “custom keyring” services—allowing consumers to choose parts and make items themselves—have become key customer-attraction content. This shows that demand for “customization,” which values individual identity, is driving sales in the low-involvement accessories market.

Gacha: The Economics of Controlled Uncertainty

Capsule toy machines and gacha shops have migrated from the back corners of underground shopping arcades to the highest-rent retail corridors in Seoul. Yeonmujang-gil in Seongsu. Major station concourses. The ground floors of premium malls.

The unit economics explain the move: 3,000 to 5,000 won per transaction, no staff, minimal inventory risk, high sales per square meter, and a repeat-visit mechanic built into the format. The consumer is paying for a small, controlled moment of uncertainty — the draw — and the brief reward of getting a character they wanted.

In a broader economic context where long-term asset accumulation feels uncertain, consumers are finding satisfaction in small wins that are actually achievable. Gacha delivers that in a low-cost, low-commitment package. Bandai's entry into the Korean market with a flagship mall format confirms that the institutional money is taking this category seriously.

The emergence of corporate-run mall formats backed by large capital—such as Bandai’s official gacha shop at Jamsil Lotte World Mall—proves that this is no temporary fad but an established retail category.

Risk Minimization: The Rise of Trial-First Retail

Paying verification costs to minimize purchase-failure risk, and ultra-small/low-volume consumption patterns

Olive Young's Olive Better format is a direct response to a consumer behavior shift: people are increasingly averse to purchase regret. As budgets tighten, the psychological cost of a failed purchase grows. Consumers are now willing to pay a verification cost — a visit to a trial-format store — before committing to a full-price purchase.

The product-level response is the ultra-small SKU: single-serve olive oil portions, travel-size incense, miniature supplements. These aren't packaging decisions. They're risk management products. They let consumers try a brand at a price point that removes the anxiety of commitment.

The demographic driver is the single-person household. Korea's single-person household rate is rising, and single consumers have no need for full-size products. They want as much as they'll actually use — nothing more. Retail formats and pack sizes that match that reality are winning. Those that are still built around family-size assumptions are not.

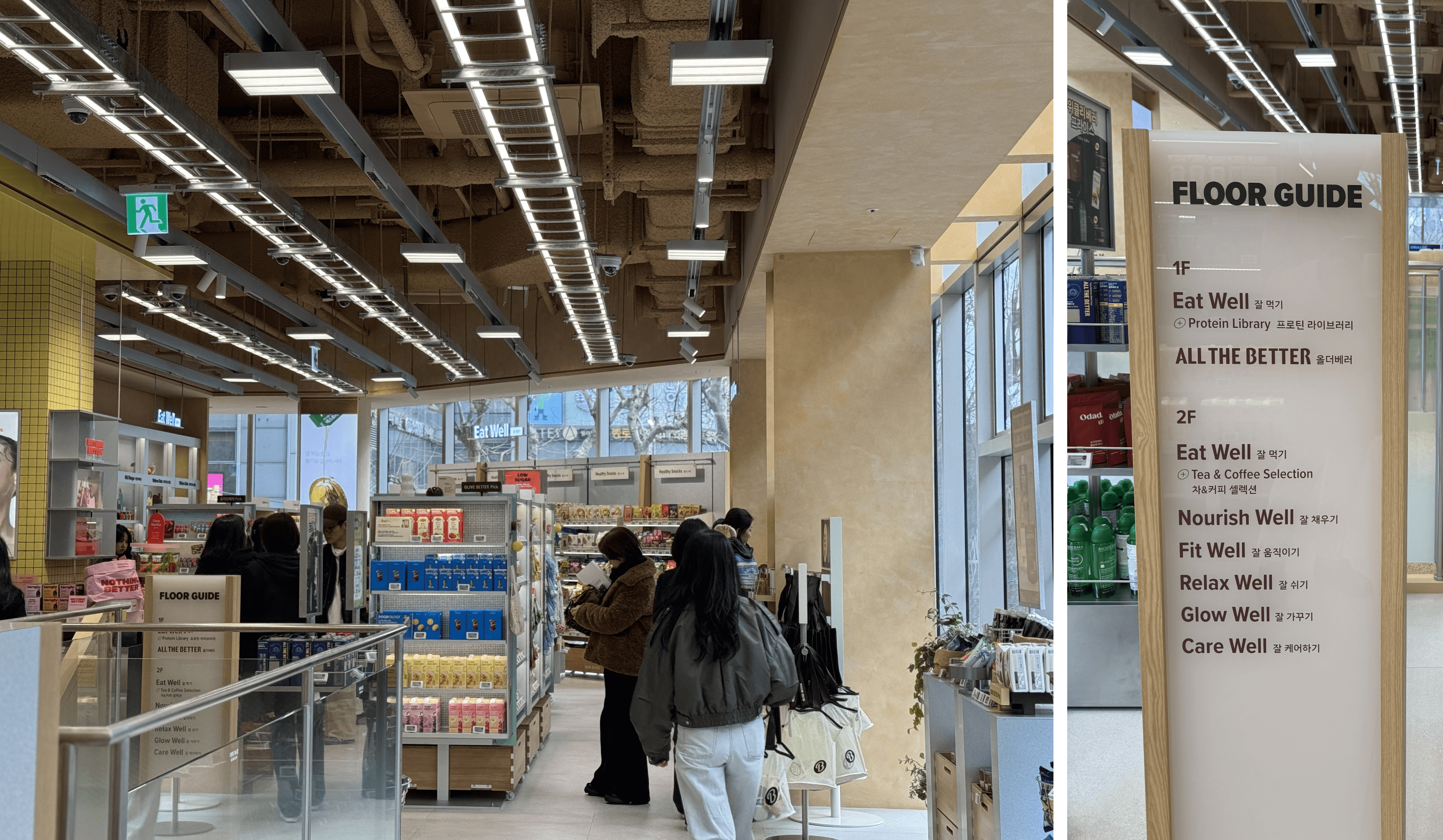

The recently opened Olive Better Gwanghwamun branch stands out for its MD composition that maximizes “high-density nutrition” and “convenience.” It curates product lines that busy office workers can easily consume during work, such as small-pack energy bars, single-dose olive oil, and supplements.

Daiso Cosmetics: The End of the Price-Quality Trade-Off

The power of real full-size products without the markup: why Daiso became a cosmetics pilgrimage spot

The conventional understanding of the beauty market assumed a correlation between price and quality. Daiso's cosmetics section is systematically dismantling that assumption.

JUNGSAEMMOOL's Daiso-exclusive line launched products at 5,000 won that had previously sold for 40,000 won under the main brand. The response was a sell-out at launch and an extended backorder period. Consumer reviews consistently reported that the quality was not proportionally lower. The price gap, it turned out, was largely brand premium — not formulation quality.

For the retail market, this is significant. If consumers can no longer assume that a higher price reflects a better product, the justification for spending at mid-tier beauty brands erodes. Daiso becomes not just a value option but a genuinely competitive alternative. That is a structural change in the category, and it will not reverse.

The color cosmetics category at Daiso’s Sports Complex Station branch shows such overwhelming turnover that securing stock on weekday afternoons is nearly impossible. As “Daiso Beauty” has moved beyond value-for-money and into the mainstream, demand is exceeding supply. Sunday morning is a golden time when stock is replenished before foot traffic surges, making it the only time to fully check the product lineup.

Golf: When the Proof Shot Gets Too Expensive

The decline of high-cost, show-off leisure and demand migration to running as a practical, high-efficiency exercise

The COVID golf boom is over. According to Korea Customs Service data, domestic golf equipment imports climbed steeply from 7,904 tons in 2019 to 12,889 tons in 2022 — then fell 3.71% year-on-year in 2023, with the January-to-August period of the following year down a further 16.49% to 7,641 tons. The pandemic-era demand surge has unwound, and the market is contracting in earnest. Reservation platform usage has peaked and reversed. The secondhand golf club market is flooded.

The underlying shift isn't just economic. Golf — and Pilates, to a similar extent — served a specific social function during the boom years: they were visible, photographable, shareable. The "proof shot" on the fairway was part of the product. Running offers none of that social scaffolding, and that's precisely the point. A pair of running shoes is all the equipment required. No green fees. No lessons. No coordinated kit. The barrier to entry is as low as it gets for a physical activity with genuine health returns.

ASICS raised its annual sales forecast to 800 billion yen in August 2025 — a figure that reflects not a domestic trend but a global demand shift away from aspirational leisure toward accessible, efficient exercise. Onitsuka Tiger's move into lifestyle sneakers that adopt technical running design elements is the same signal from a different angle: the "running-core" aesthetic, where performance vocabulary crosses into everyday fashion, is now a commercial category in its own right.

Onitsuka Tiger joined the trend by launching lifestyle sneakers that adopt the functional design of professional running shoes. This is an outcome of the “running-core” trend, in which the popularization of serious running has expanded into fashion. By translating technical elements of performance shoes into everyday fashion items, the brand is targeting highly involved consumers who pursue both functionality and style.

Insight: You only need One.

A tougher economy doesn't eliminate desire. It changes the channel it flows through.

The era of status signaling through big-ticket purchases — imported cars, luxury handbags, golf club memberships — has cooled, at least for the median consumer. What's replaced it is something more precise: a clear sense of where personal value actually sits, and a willingness to spend freely there while cutting aggressively everywhere else. The unit of indulgence has shrunk. The intentionality behind it has grown.

At lunch, budget coffee. On the way home, a customized pen or an 8,000-won cookie — not because the consumer can't afford better coffee, but because the cookie is where the enjoyment is concentrated today. The logic isn't deprivation. It's editing.

Running shoes by the Han River instead of a weekend tee time. Ultra-small product formats to test before committing. Gacha for the thrill of the draw at 4,000 won. These aren't consolation behaviors. They're optimized ones. Consumers have become very good at finding the highest-return moment within a constrained budget, and they're executing that search with real precision.

For retail, the implication is uncomfortable but clear. Volume and visibility no longer guarantee relevance. The brands that survive this period of fragmented, polarized, precision consumption are the ones that can deliver a genuinely felt moment — something small enough to be affordable, specific enough to feel chosen, and real enough to be worth it. The logo is optional. The detail is not.

© Copyright 2026. All rights reserved.

This publication has been prepared in good faith, based on CBRE Korea's current anecdotal and evidence based views of the commercial real estate market. Although CBRE Korea believes its views reflect market conditions on the date of this presentation, they are subject to significant uncertainties and contingencies, many of which are beyond CBRE Korea’s control. In addition, many of CBRE Korea’s views are opinion and/or projections based on CBRE Korea’s subjective analyses of current market circumstances. Other firms may have different opinions, projections and analyses, and actual market conditions in the future may cause CBRE Korea’s current views to later be incorrect. CBRE Korea has no obligation to update its views herein if its opinions, projections, analyses or market circumstances later change.

Nothing in this publication should be construed as an indicator of the future performance of CBRE’s securities or of the performance of any other company’s securities. You should not purchase or sell securities-of CBRE or any other company-based on the views herein. CBRE Korea disclaims all liability for securities purchased or sold based on information herein, and by viewing this publication, you waive all claims against CBRE Korea as well as against CBRE Korea’s affiliates, officers, directors, employees, agents, advisers and representatives arising out of the accuracy, completeness, adequacy or your use of the information herein. No part of this publication may be reproduced, quoted, distributed, or disclosed to any third party without the prior written consent of CBRE Korea.

trend

Jul 6, 2026

The footsteps of runners change the commercial districts

Runners' Basecamp: SEOUL's second article, commercial districts transformed by runners centering around Seochon and Bukchon

trend

Apr 20, 2026

Then it was bags, now it is jewelry.

"Rather than buying a 14 million won bag..." Consumers start 'Open Runs' at 'this place'

trend

Apr 13, 2026

The Secrets Behind the Success of Eulji Kankan

Appeared in Culinary Class Wars Season 2, Representative Cho Kyung-chan of Eulji KkanKkan—who brought the taste of real, local Vietnam to Korea—talks about his laws of entrepreneurship, space, and expansion.

trend

Apr 13, 2026

Runners' Basecamp: SEOUL

UVU chose Seongsu over London for its world-first store — how Seoul's running scene is redrawing the retail map.

trend

Apr 13, 2026

Pharmacy or Olive Young?

How K-pharmacy became Seoul's most unexpected anchor tenant category.