Back

Share

Like

market

Article Highlights

Location alone is no longer enough; performance gaps now stem from operational design.

Foreign consumers are active taste-makers, redefining retail space and content strategies.

Brands build digital fandoms first, but physical space remains the ultimate tool to solidify brand experience.

The old rule

For a long time, retail real estate had one absolute rule. If you secure a prime location, the rest will follow. High scores in foot traffic data, visibility, and accessibility were seen as a guarantee for success. Tenants bought location, and landlords sold location.

That rule is no longer working. Even in the same commercial district and similar locations, performance gaps among brands are widening. While location clearly remains an important variable, an increasing number of cases cannot be explained by location alone. The key is not the space itself, but how that space is designed and operated.

Anatomy by Commercial District: Same Seoul, Different Equations

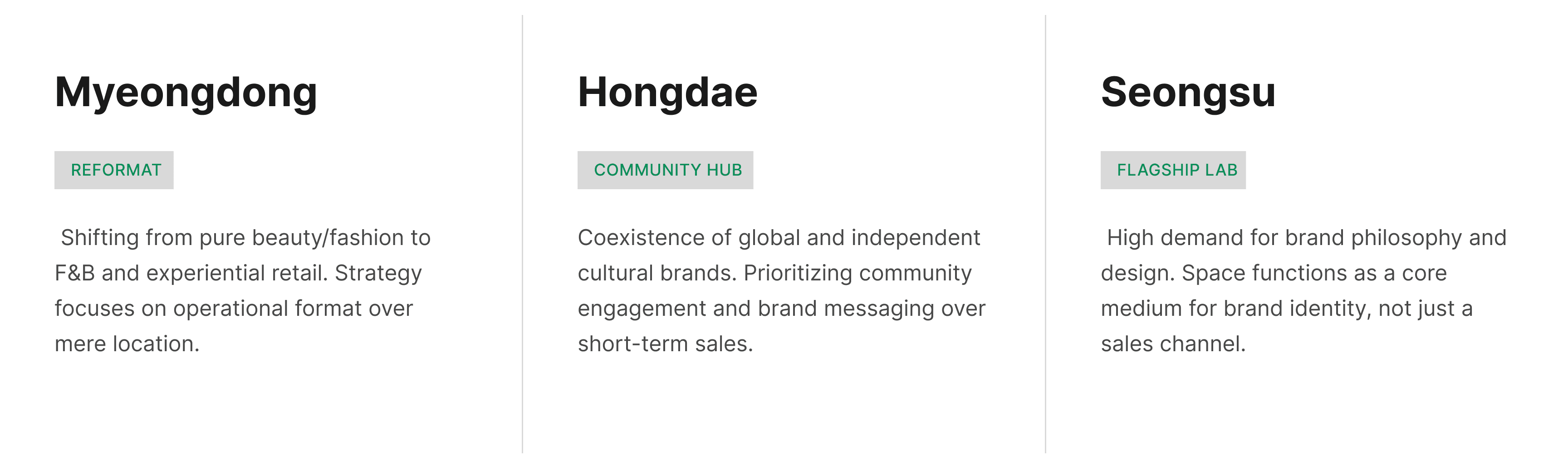

Currently, Seoul's major commercial districts—Myeongdong, Hongdae, and Seongsu—are experiencing this transition in distinct ways. On the surface, they all seem to be undergoing a 'recovery', but the nature of the internal reorganization is completely different.

While Myeongdong is a district of 'realignment,' Seongsu is one of 'experimentation.' Meanwhile, Hongdae lies somewhere in between, where local identity and global brands coexist in a peculiar balance. All three commercial districts share the commonality of having shifted their competitive edge from "where you are located" to "how you exist."

Structural Shift: How the Pandemic Changed the Reason for Offline Existence

The roots of this change lie in the pandemic. As shopping shifted online, offline space was redefined not as 'a place to buy things' but as 'a space to spend time and accumulate experiences.' Consumers have already learned that buying online is faster and more convenient. So, what should offline spaces do?

The answer is to create a motive for visiting and to offer dwell value. As 'what experience was had' began to lead to stronger memories and sharing than 'what was bought,' young consumers in particular evaluate brands based not just on products, but on the atmosphere, stories, and methods of engagement created within the space. Accordingly, the competitiveness of commercial districts has shifted. The issue is no longer the sheer volume of foot traffic, but whether there is a reason for visitors to linger or whether a structure is in place for content to circulate.

Expert's Insight

"This is why the current local commercial districts feel less like they are in a 'recovery phase' and more in a state of 'structural reorganization.' Even if external demand returns, spaces that lack an operational structure cannot capture that demand. Retail spaces are no longer staying as objects of lease or sales channels; they are being redefined as 'operable platforms' where brand strategies are brought to life."

A New Perspective on Assets

The perspective of landlords is also changing. Moving away from evaluations centered solely on vacancy rates and rental yields, they are expanding their scope to assess the brand experience and operational potential that a space can offer.

In the past, arcades were considered mere annexes to office buildings. Today, they are increasingly redefined as independent content-driven commercial hubs. Gran Seoul strategically introduced Starfield Avenue, restructuring the commercial area around brand curation and customer flow designed to encourage lingering. One Sentinel also reorganized its retail section into a primary driver of asset value through spatial expansion and MD adjustments. These cases demonstrate that even assets with physical limitations can be redefined through content strategies and operational design.

Another change is the method of securing stability in tenant structures. As medical retail takes on the role of absorbing vacancy risks on upper floors, major commercial districts like Gangnam-daero have seen an influx of medical practices even into spaces formerly used as offices. This suggests that combining target anchor tenants with steady demand, rather than short-term trend-heavy businesses, has become a core challenge in asset management.

Near Gangnam Station. One of the areas where changes in the commercial district have been prominent since the COVID-19 pandemic.

Foreign Demand Transforms Spatial Design

The recovery of foreign tourist demand has gone beyond a mere increase in foot traffic; it is practically changing the criteria for planning and operating retail spaces. While foreign consumption in the past was focused on 'shopping' in Myeongdong before departure, recent demand is clearly focused on "what brand to experience, in what way, and how to capture that experience as content." Indeed, it is now very common for foreign visitors to personally reserve fine dining or unique bars in Korea, or seek them out via social media.

Therefore, foreign demand visiting Korea is closer to 'consumers' exploring new brands and curating their own tastes rather than simple 'tourists.' This is why we see a highly sensitive response to "formats where experiences can be designed," such as independent brand showrooms, collaborative pop-ups, and conceptual flagship stores. Brands, too, increasingly tend to operate spaces as hubs for building touchpoints with global customers, rather than just generating short-term sales.

There is no place where conceptual competition among brands is as fierce as Seongsu-dong. From 2025 onwards, consumption by foreigners in Seongsu is projected to surpass that of locals.

Tenants' Decision-Making Has Changed

The biggest change in practice is that tenants no longer regard commercial districts merely as places with high foot traffic. They evaluate based on visitor demographics, movement patterns, and the role their brand can play within that district.

In Dosan-daero, high-sensitivity F&B and lifestyle brands strongly tend to review store openings on the premise of content productivity and spatial branding. Rather than simple visibility, they focus on the brand experience and the power of the message the space can deliver. In Hannam, as curation-type spatial strategies intensify around global fashion brands and select shops, factors like brand combinations, the quality of dwell time, and the symbolic value within the district play a larger role in store placement decisions.

Expert's Insight

"Because the way results are generated has changed even within the same 'core commercial district,' changes are appearing in the decision-making structure. Unlike in the past when store openings were decided primarily by sales or store development teams, marketing, brand, and content organizations are now involved from the early stages, placing a heavier weight on whether 'this space can fully embody the brand's identity' as a key criterion."

Another shift is the demand for physical and operational flexibility in spaces. Modern stores are not built once and left as they are; they are operated to be continuously updated in line with seasons, content, and campaigns. Even from the pre-contract stage, there is a clear increase in how often operational reviews assess whether a space can accommodate content, whether its structure allows for staging and modifications, and whether it accommodates filming, interactive elements, visual exposure, and interior traffic design.

The Quiet Reorganization of Local Commercial Districts

While Seoul's core commercial districts have naturally formed around foot traffic and infrastructure, local districts and new-town mixed-use developments exhibit a clearer structure where specific assets become the central hubs or actively shape the commercial area. CBRE interprets this trend as an 'asset-driven commercial district transition.' Rather than an asset being absorbed into an existing district, it redefines the nature of the district itself by serving as a new axis of consumption in the area through lifestyle, leisure, and cultural functions that encourage dwell time and repeat visits.

As local commercial districts transition from 'naturally occurring' to 'planned and operated,' tenant strategies must also move away from foot-traffic-centric approaches. The key lies in creating functional connections with the local community and designing a tenant mix that sparks synergies between business types. Ultimately, success in local districts is heavily determined by whether we can design an operational structure that generates repeat visits within the daily rhythm of local life.

Where is the Next Commercial District?

There are places that hold value missed by conventional, foot-traffic-centered market analysis. Seochon, Bukchon, and Euljiro are prime examples.

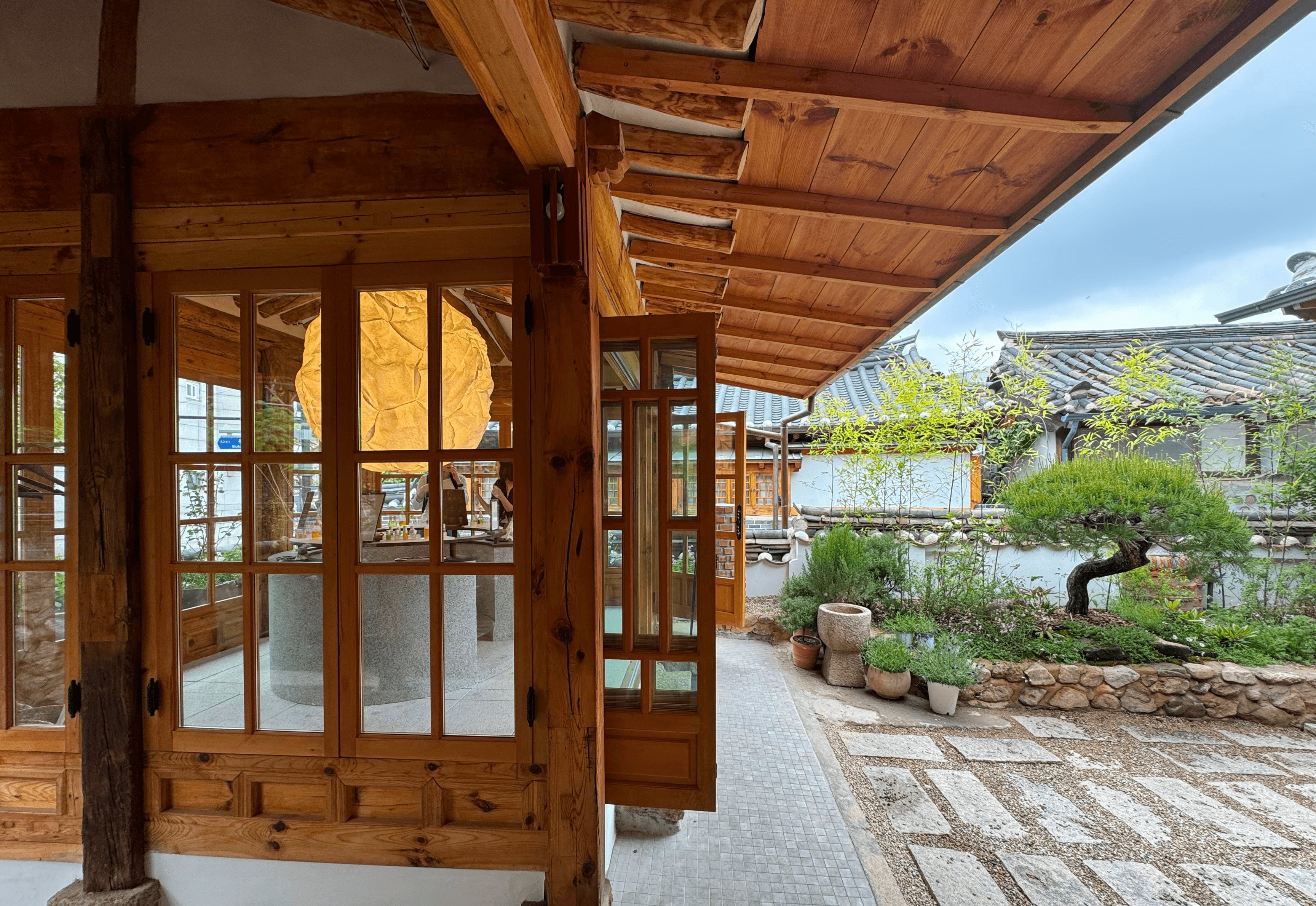

Seochon's greatest asset is the tranquility provided by low-rise buildings and topography that resists artificial, large-scale development. Independent brands and galleries nestled in its alleys have formed a solid community, offering the perfect stage for a brand to calmly unfold its authentic storytelling. In Bukchon, there is constant demand for flagship locations from global brands seeking to modernly reinterpret the aesthetics of Hanoks (traditional Korean houses). It serves as a strategic choice to elevate a brand's prestige.

Aromatica Hanok store. An example of how the structure and materials of a hanok became the most effective medium to embody the brand's philosophy.

One of the alleys attracting the highest concentration of foreigners in Seoul. This scene of multinational visitors lining up under the narrow eaves of Hanoks proves that Bukchon is not just a tourist destination, but a rare stage where brands can directly connect with global consumers.

With land values and rents in main districts like Seongsu-dong soaring recently to create a strict landlord-dominated market, brands fatigued by this are pivoting their retail strategy toward purchasing rather than leasing. In particular, Bukchon and Seochon are emerging as strong alternative investment destinations because their price per square meter is reasonable compared to core areas that have already seen price explosions. Furthermore, the small parcel sizes located between alleys reduce the total purchase burden. As the strategic decision to secure brand longevity by escaping gentrification risk aligns with the unique, quiet aura and historical narrative of Bukchon and Seochon, the movement of brands looking to own their buildings and establish sophisticated flagship hubs is growing even faster.

Euljiro is currently showing the most dynamic changes, coupled with the retail repositioning strategies of large office assets. Once mere dining areas, the lower arcade spaces of office buildings are rapidly evolving into high-sensitivity content hubs that simultaneously appeal to both office workers and Gen Z. It is a unique hybrid market where the stability of office background demand meets the explosive potential of diverse content.

Gran Seoul is a representative case that strategically integrated Starfield Avenue, reconstructing the commercial area's character focused on brand curation and customer flow designed to encourage lingering.

In particular, Cheonggyecheon is a crucial axis that completes the dynamics of Euljiro's office retail repositioning. This is because the Cheonggyecheon waterfront, which once disconnected commercial districts, now functions as a natural access route and a crowd-puller, channeling huge holiday and weekend crowds into prime office lower levels. As the analog vibes of Hipjiro and the sophistication of large buildings organically intersect along Cheonggyecheon, Euljiro is evolving into an irreplaceable hybrid location where the stability of weekday office districts and the explosive energy of weekend waterfront areas coexist.

Independent F&B and select shops, permeating between old printing houses and hardware stores, are creating a new axis of consumption. This scene displays the unique hybrid location of Euljiro, where the stability of the weekday office market and the explosiveness of the weekend waterfront market coexist.

These three commercial districts share one commonality: they offer a 'context' in which brands can build emotional bonds with consumers and cultivate a long-term fandom. Rather than simple high-foot-traffic areas, places where visitors can deeply experience a brand's message within the local context are taking center stage.

And Going Global

Rue des Francs Bourgeois, Le Marais (3rd/4th Arrondissement). One of the streets in Paris where the most concentrated brand experiences are condensed.

Finally, as competition in the domestic retail market reaches its peak, brands are setting their sights completely beyond national borders. Interestingly, global expansion is no longer merely the next step taken after securing domestic success. Recently, some high-sensitivity emerging brands bypass launching in the Korean market initially, instead targeting overseas consumers first with a global launch before entering Korea in reverse. The digitalized global market is no longer a challenging stage blocked by physical distance or capital limitations; it has become possible to first verify global consumer responses through data and build a fandom via e-commerce and digital cross-border platforms without opening large local brick-and-mortar stores.

However, even as the stage expands infinitely to global screens, the power of physical space to fully convey a brand's philosophy and depth can never be replaced. While digital channels can raise product awareness and drive sales, only offline spaces can perform the essential task of imprinting a brand's depth and heritage through sensory experiences. Paradoxically, even brands that have conquered global markets first put effort into establishing physical hubs in overseas regions. Rather than rolling out a large number of stores, they seek to show the essence of their brand and complete the density of the experience by presenting a single, elaborately planned space in key global hubs. Ultimately, even for brands that have lowered global market barriers through digital means, physical space still serves as the most powerful and essential tool to initiate and complete their branding.

© Copyright 2026. All rights reserved.

This publication has been prepared in good faith, based on CBRE Korea's current anecdotal and evidence based views of the commercial real estate market. Although CBRE Korea believes its views reflect market conditions on the date of this presentation, they are subject to significant uncertainties and contingencies, many of which are beyond CBRE Korea’s control. In addition, many of CBRE Korea’s views are opinion and/or projections based on CBRE Korea’s subjective analyses of current market circumstances. Other firms may have different opinions, projections and analyses, and actual market conditions in the future may cause CBRE Korea’s current views to later be incorrect. CBRE Korea has no obligation to update its views herein if its opinions, projections, analyses or market circumstances later change.

Nothing in this publication should be construed as an indicator of the future performance of CBRE’s securities or of the performance of any other company’s securities. You should not purchase or sell securities-of CBRE or any other company-based on the views herein. CBRE Korea disclaims all liability for securities purchased or sold based on information herein, and by viewing this publication, you waive all claims against CBRE Korea as well as against CBRE Korea’s affiliates, officers, directors, employees, agents, advisers and representatives arising out of the accuracy, completeness, adequacy or your use of the information herein. No part of this publication may be reproduced, quoted, distributed, or disclosed to any third party without the prior written consent of CBRE Korea.

market

Apr 13, 2026

It starts with data and is completed in the field

The Essence of the 2026 Retail Market, According to CBRE's Head of Research

market

Apr 13, 2026

The End of Strata Retail?

Supply is down on paper. Vacancies are up on the ground. The hidden oversupply and structural flaw behind Korea's pre-sale retail crisis.

market

Apr 13, 2026

Two Years Locked in Permits

The real cost of overseas retail expansion without a project management framework — why permit risk has to be resolved before the lease is signed.

market

Apr 13, 2026

From Supporting Role to Lead: Office Retail

From basement canteen to asset value driver — fifteen years of structural change in Seoul's office building retail, from Centre One to Olive Young N Seongsu.

market

Apr 13, 2026

Why Gut Instinct Kills Your Flagship Store

Thirty-one retail real estate practitioners rank what actually determines flagship store performance.

market

Apr 13, 2026

Know Anyone Good to Set Me Up With?

How leasing decisions are actually made in Seoul's most competitive retail districts — and why the broker in the middle determines the outcome.

market

Apr 13, 2026

New Era, New Areas

Korean brands are going global. The ones that make it understand one thing first: overseas leasing is a credit game, not a rent game.

market

Apr 13, 2026

It's Not That They're Not Spending

Why foreign visitor spending data is replacing card transactions as the next frontier in retail intelligence.

market

Apr 13, 2026

You are so Beauti-cal

Dermatology clinics are now the most sought-after anchor tenants on Gangnam street

market

Apr 13, 2026

Reading a Brand's DNA Before They Do

The retail MD practitioner's job is translation — turning a brand's qualitative language into measurable spatial conditions. What that looks like in practice.