Back

Share

Like

market

Article Highlights

2026 market polarization will widen the gap between prime and secondary assets despite stable vacancy rates.

Retail real estate indicators are now lagging behind actual retailer data and trends.

As office supply surges, arcade spaces must evolve from basic amenities into destination hubs to differentiate assets.

Official data points to a recovery. The vacancy rate for Grade A offices in Seoul is in the 3% range, commercial real estate transaction volume reached an all-time high of 33.8 trillion KRW, and the vacancy rate in Myeongdong has also improved to the 8% range from the 50% range in 2021. Looking at the numbers alone, it reads as if the market has fully normalized. However, the temperature on the ground is different. What the indicators hide, why it is difficult to treat the retail market solely with numbers, and why the office arcade is becoming a key keyword for retail at this point in time. We hear this story directly from Claire Choi, Head of Research at CBRE Korea.

Polarization, the Real Battle After Vacancy Stabilization

The Seoul commercial real estate market has changed noticeably over the past two years. In 2025, the overall transaction volume reached an all-time high of 33.8 trillion KRW, and vacancies stabilized across all sectors, including office, logistics, and retail. However, Head of Research, Claire Choi looks at these figures a bit differently.

Q. Is there a key theme that runs through the entire 2026 Outlook report?

If I had to choose just one, it would be polarization. This is a trend observed across the board, including retail, in both the leasing and investment markets. Currently, demand in high street retail markets practically relies heavily on tourists. Domestic consumption is not in a particularly good state. Nevertheless, retail leasing activities in Seoul are actively occurring, and this part certainly has a gap with macroeconomic indicators.

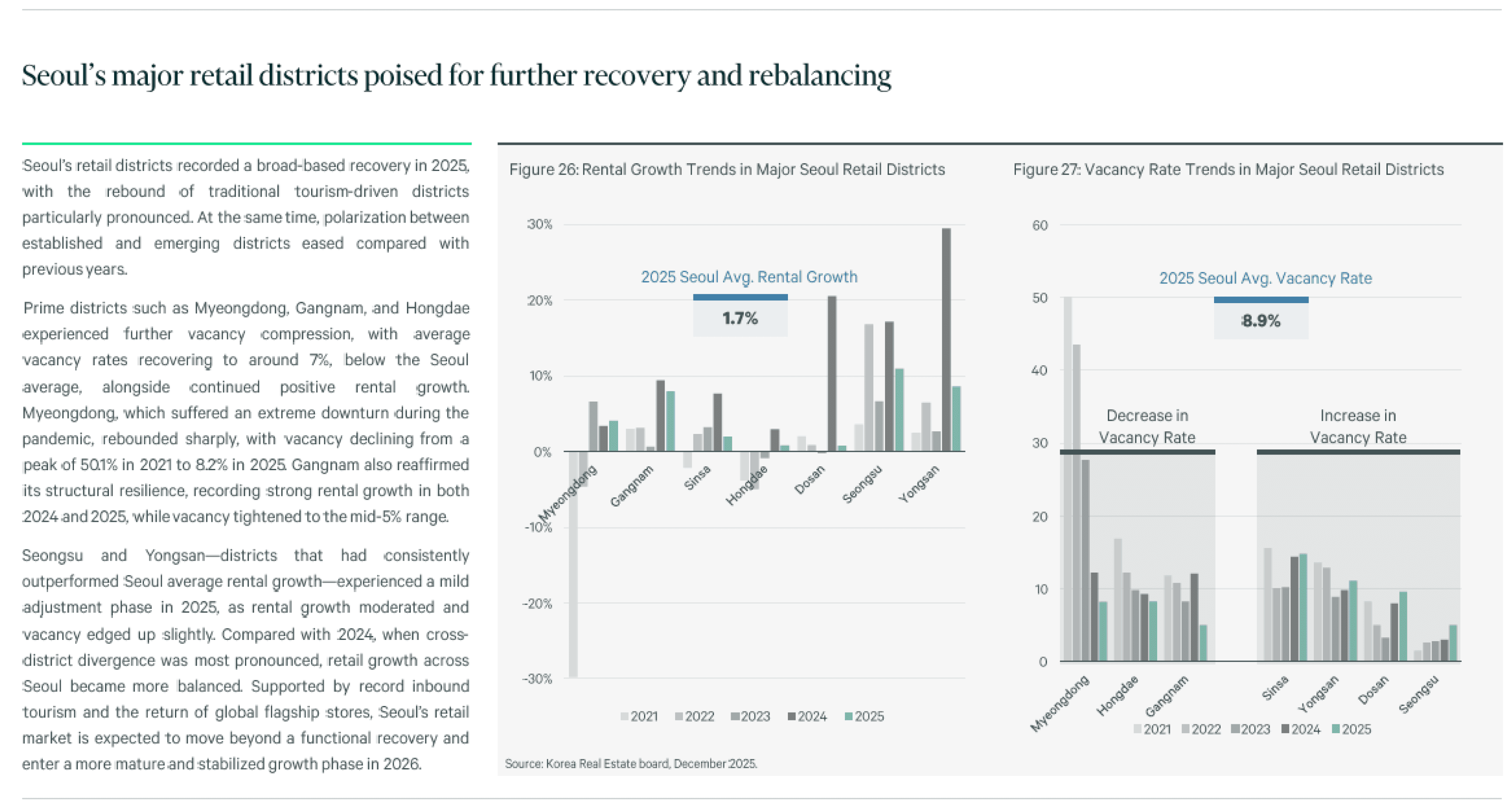

In the end, it means that prime retail areas are doing well, while other areas are still struggling. Garosu-gil is still facing difficulties, whereas core commercial areas like Gangnam and Myeongdong recovered quickly. It is true that vacancies have stabilized to some extent. However, I believe we have now entered a phase of separating the wheat from the chaff, identifying which assets will continue to perform well in the future and which will not.

2026 Real Estate Market Outlook: Based on major commercial areas in Seoul in 2025, the vacancy rate in Gangnam fell to the 5% range, recording a 4.0% year-on-year rent increase. On the other hand, Seongsu and Yongsan entered a minor adjustment phase as rental growth slowed. Myeongdong's vacancy rate recovered to 8.2% from 50.1% in 2021. (CBRE Research, 2025)

Q. Was there anything that turned out differently from your expectations while writing the report?

The report is prepared in December and published in early January, but the market can change significantly even during that short period. At the time of writing, the prevailing forecast was that interest rates would be cut once this year, but at the time of publication, the direction suddenly shifted to predominantly trend-less/neutral. Now, other variables like Middle East risks are emerging.

In fact, there have been large and small variables every year—MERS, THAAD, and COVID-19. Therefore, I believe it is correct to use reports not as predictive books that exactly match reality, but as tools to read the market's direction.

The Limits of Reading Retail Through Numbers

For offices, it's vacancy rates and rents; for logistics, it's net absorption and the supply pipeline. The framework for reading the market with quantitative indicators is relatively clear. Retail is different. This is because it is a market where the asset value changes entirely depending on which floor it is, or which brand is moving in, even within the same building.

Q. From a research perspective, what is the most different approach you take for retail compared to other sectors?

Retail is a market that is difficult to approach from a purely real estate perspective. Ultimately, retailer and tenant demand trends come before real estate indicators. The key is which brands are leading the market and where consumption patterns are moving. Therefore, we communicate and collaborate closely with the retail team on a regular basis. We take macroeconomic indicators and cross-check how they are actually felt on the ground.

While the research team is responsible for macroeconomic trends and figures, the retail team possesses much more detailed and immediate on-the-ground data. Which brand wants to enter where, and how the temperature of a specific commercial area is changing. These are the parts we struggle to capture through statistics. It is difficult to properly understand the retail market without those details from the field.

Q. You utilize a lot of indirect indicators such as the Consumer Sentiment Index and card transaction volumes. How do you bridge the gap between macro data and the actual retail districts?

To be honest, it is difficult to completely bridge that gap. We look at open data, such as retail sales trends by store type, the Consumer Sentiment Index, and card transaction volumes from various angles to read the direction. Instead of separating domestic and foreign demand, we focus on the overall size trend of the retail sales market.

Adding the real feel of the field on top of that is the role of the retail team. If macro data points to a direction, the retail team knows what is actually happening inside that trend. I believe that only when these two perspectives mesh can we truly look at the market in a multi-dimensional way.

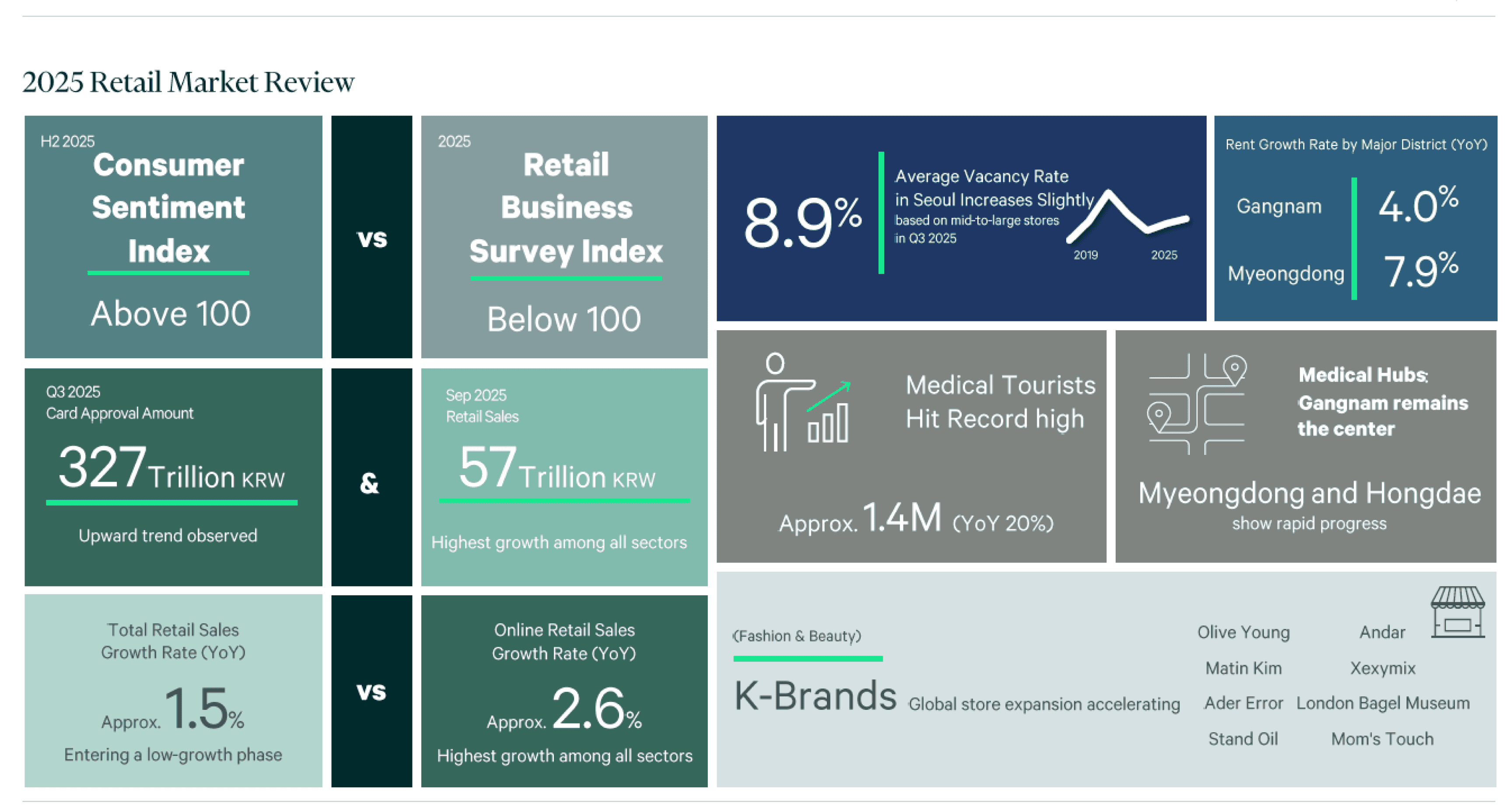

2026 Real Estate Market Outlook: The change in overall retail sales in 2025 entered a low-growth phase at approximately +1.5%. Only online channels maintained growth for six consecutive years, while most offline store types remained flat or declined. Although the Consumer Sentiment Index exceeded 100, the Retail Business Survey Index remained below 100, continuing the difference in temperature between suppliers and consumers.

Office Arcades, Transformed from Ancillary Facilities to Destinations

Q. I am curious about your intention in focusing heavily on office arcades in this report. From a research standpoint, is an arcade an ancillary facility of an office, or an independent retail asset?

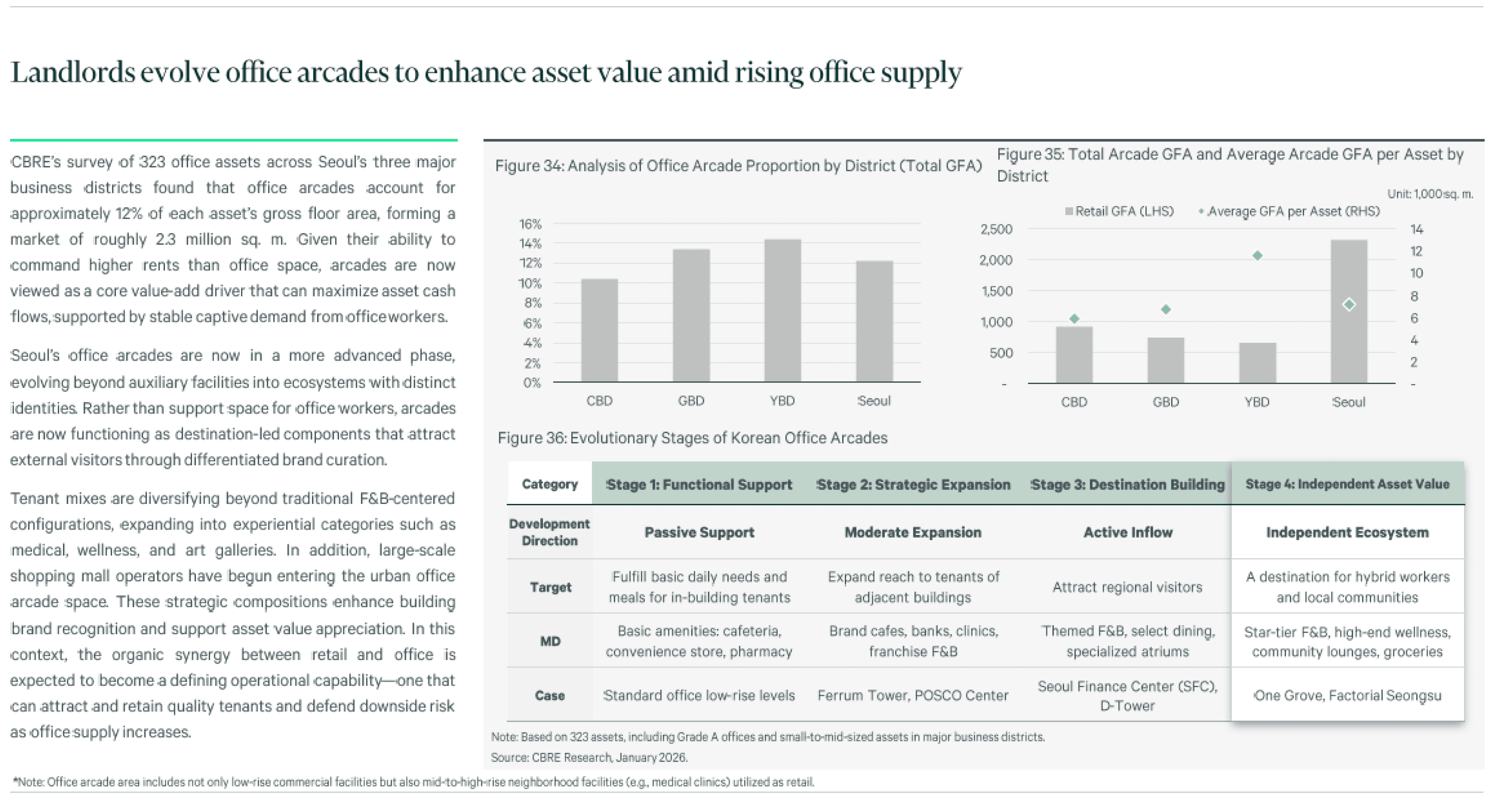

The supply of offices in Seoul will begin to increase in earnest going forward. Under the assessment that arcades will be the key to asset differentiation in that competitive environment, we intentionally covered it in this report.

Basically, retail in an office is indeed an ancillary facility. The primary demand for an arcade comes from the office tenants. Even when vacancies in high street retail exploded during COVID-19, arcades remained relatively stable. This is because there is always a base demand from the working population supporting them. In the case of F&B, the demand to enter prime arcades is consistently strong.

However, its role is now evolving. The mix, which in the past centered on convenience stores and cafeterias, has changed today to encompass Michelin-starred restaurants, high-end wellness, and groceries. It has begun to function as a destination that draws external visitors. The entry of Starfield into a downtown office at Gran Seoul for the first time, and Maseok One Grove recording a 95% occupancy rate during its initial opening phase, both demonstrate this trend well.

2026 Real Estate Market Outlook: According to a complete survey of 323 office assets in Seoul's three major business districts, arcades account for an average of about 12% of the gross floor area, forming a market of approximately 2.3 million square meters across Seoul.

Q. As arcades become more sophisticated, couldn't they potentially cannibalize the surrounding high street commercial areas?

I believe it is quite the opposite. Euljiro is a good example. As new offices are built, arcades are expanding as well, and this is leading to an effect that lifts the entire Euljiro commercial area. It is a structure where offices increase floating population, arcades absorb that demand, and the surrounding high street retail districts also benefit together.

The same goes for Seochon and Bukchon, which are within walking distance of the CBD. The quality of a working environment is not determined solely inside the building. It includes where you can walk during lunch transit, and what kind of spaces are nearby. In that sense, office arcades and surrounding high street retail areas have more of a synergistic relationship rather than a competitive one.

A Commercial Area Walked Directly by the Research Head

Q. As a research head, is there a commercial area or shift that you personally find most interesting these days?

These days, I can really feel that the area around Euljiro has changed a lot. As new offices continue to be built, the surrounding commercial areas are changing as well. What was once purely a office worker lunch district is transforming into a space that people visit during evenings and weekends as well.

This is also true for Seochon and Bukchon, which are walkable from the CBD. I had a meal near Bukchon recently, and the atmosphere had changed significantly. More supply of new offices is scheduled for this area, and arcades will expand. Personally, I am watching with interest to see what kind of changes that will bring to the surrounding commercial districts.

Looking at these areas, I reaffirm that the quality of a workspace is not completed solely within a building. Alleyways you can walk to during lunch, spaces you can stop by after work. Prime offices enter places equipped with such environments, and when prime offices enter, the surroundings change again. As new offices and arcades are added to this district in earnest going forward, I am personally paying close attention to how far that change will reach.

Bukchon crowded with tourists. Attention is focused on what kind of synergy will be created in connection with not only tourists but also the supply of new offices in the surrounding area.

The retail market is not entirely read through data alone. The status of a building changes depending on which brand moves in, and the temperature of surrounding alleys shifts as a single office is established. That is why even the Head of Research says, "It is difficult to understand without experts on the ground." Now that indicators point to a recovery, it is time to have an eye to see which assets possess true competitiveness behind those numbers.

© Copyright 2026. All rights reserved.

This publication has been prepared in good faith, based on CBRE Korea's current anecdotal and evidence based views of the commercial real estate market. Although CBRE Korea believes its views reflect market conditions on the date of this presentation, they are subject to significant uncertainties and contingencies, many of which are beyond CBRE Korea’s control. In addition, many of CBRE Korea’s views are opinion and/or projections based on CBRE Korea’s subjective analyses of current market circumstances. Other firms may have different opinions, projections and analyses, and actual market conditions in the future may cause CBRE Korea’s current views to later be incorrect. CBRE Korea has no obligation to update its views herein if its opinions, projections, analyses or market circumstances later change.

Nothing in this publication should be construed as an indicator of the future performance of CBRE’s securities or of the performance of any other company’s securities. You should not purchase or sell securities-of CBRE or any other company-based on the views herein. CBRE Korea disclaims all liability for securities purchased or sold based on information herein, and by viewing this publication, you waive all claims against CBRE Korea as well as against CBRE Korea’s affiliates, officers, directors, employees, agents, advisers and representatives arising out of the accuracy, completeness, adequacy or your use of the information herein. No part of this publication may be reproduced, quoted, distributed, or disclosed to any third party without the prior written consent of CBRE Korea.

market

May 26, 2026

2026 Retail Market Insights from the Head of CBRE Korea Retail

From Seoul to the globe, the variable determining the success or failure of retail spaces is shifting from 'where' to 'how'.

market

Apr 13, 2026

The End of Strata Retail?

Supply is down on paper. Vacancies are up on the ground. The hidden oversupply and structural flaw behind Korea's pre-sale retail crisis.

market

Apr 13, 2026

Two Years Locked in Permits

The real cost of overseas retail expansion without a project management framework — why permit risk has to be resolved before the lease is signed.

market

Apr 13, 2026

From Supporting Role to Lead: Office Retail

From basement canteen to asset value driver — fifteen years of structural change in Seoul's office building retail, from Centre One to Olive Young N Seongsu.

market

Apr 13, 2026

Why Gut Instinct Kills Your Flagship Store

Thirty-one retail real estate practitioners rank what actually determines flagship store performance.

market

Apr 13, 2026

Know Anyone Good to Set Me Up With?

How leasing decisions are actually made in Seoul's most competitive retail districts — and why the broker in the middle determines the outcome.

market

Apr 13, 2026

New Era, New Areas

Korean brands are going global. The ones that make it understand one thing first: overseas leasing is a credit game, not a rent game.

market

Apr 13, 2026

It's Not That They're Not Spending

Why foreign visitor spending data is replacing card transactions as the next frontier in retail intelligence.

market

Apr 13, 2026

You are so Beauti-cal

Dermatology clinics are now the most sought-after anchor tenants on Gangnam street

market

Apr 13, 2026

Reading a Brand's DNA Before They Do

The retail MD practitioner's job is translation — turning a brand's qualitative language into measurable spatial conditions. What that looks like in practice.