Back

Share

Like

market

Article Highlights

The retail strata-sales(Sectional Ownership) market is reaching a breaking point due to untracked supply from KIC retail units and mixed-use commercial blocks, which remain outside the scope of official data.

Korea's project financing structure creates a self-perpetuating cycle. Retail space is built to serve the financing model, not the occupier. The oversupply problem is structural, not cyclical.

This is not the end of retail investment in Korea. It is the beginning of a more discerning market. Only assets with proven anchor tenants and genuine catchment fundamentals will hold their value.

The Cold Wind Blowing in the Strata-Retail Market

Official data indicates a reduction in supply, but the field is suffering from unprecedented vacancy fatigue. Where does this gap come from?

The headline numbers say supply is tightening. Walk through almost any suburban commercial development in Korea and the reality is different: shuttered units, struggling tenants, vacancy fatigue that has been accumulating for years. The gap between the official data and the ground isn't a measurement error. It's a structural problem — one that runs through the way retail space is built, financed, and sold in Korea. Andrew Ji, Senior Managing Director at CBRE Korea's Retail Team, explains what's actually driving the oversupply and where the market goes from here.

he Hidden Oversupply: How the PF Model Creates Retail That Nobody Needs

Official commercial land statistics show a shrinking supply pipeline. What they miss is everything that doesn't get counted: retail podiums in knowledge industry centers, ground-floor units in mixed-use residential towers, café streets built into resettlement zones. None of these show up in the headline numbers. All of them absorb tenant demand.

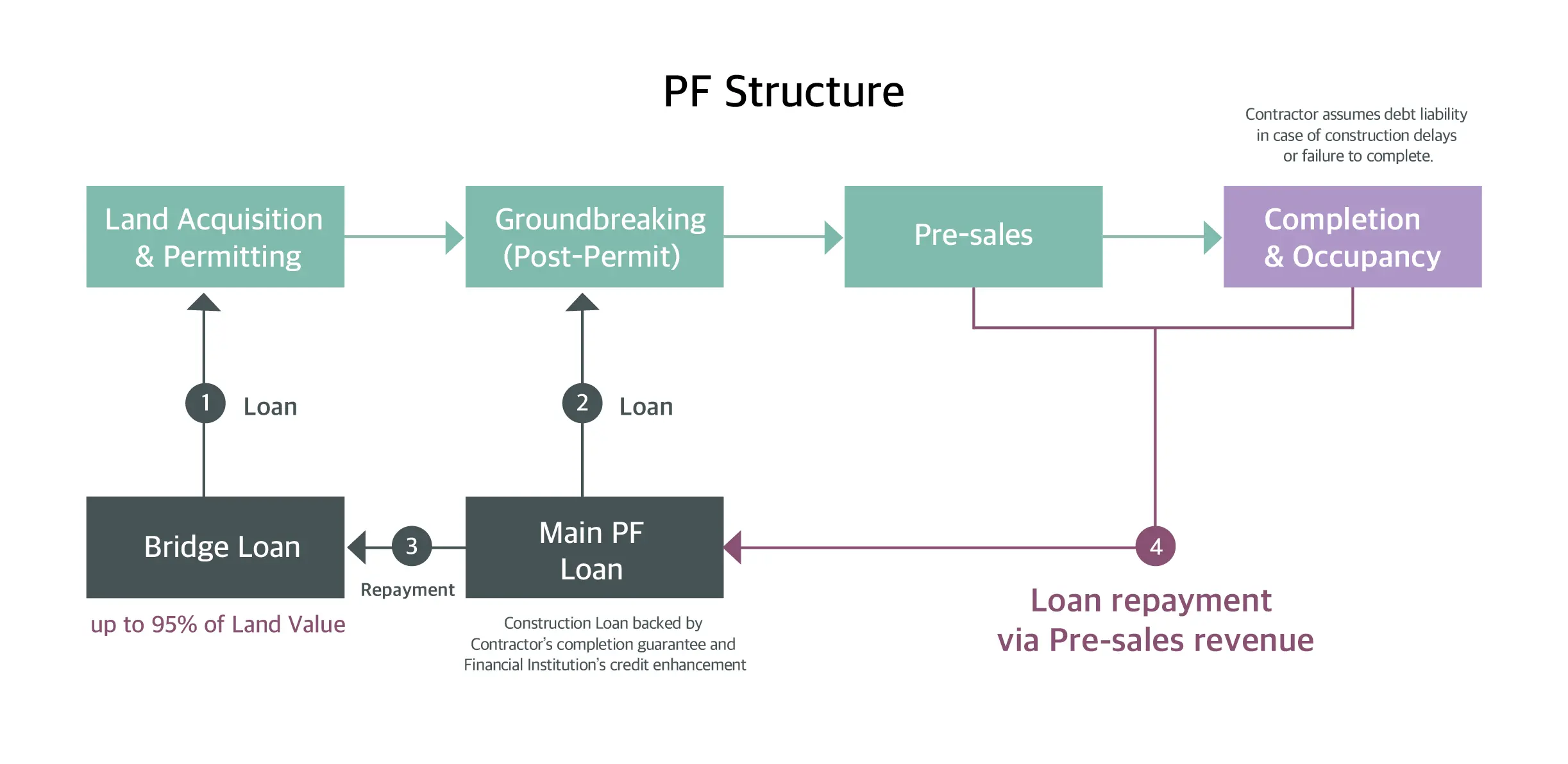

The underlying driver is Korea's project financing structure. Developers typically operate with very low equity and high leverage. To service that debt during construction, they need cash — and the fastest way to generate it is to pre-sell retail units. So retail space gets built not because there's occupier demand, but because the financing model requires it. The result is chronic oversupply that has nothing to do with the market and everything to do with how projects get funded.

Q. Why has strata retail been so persistent as an investment model in Korea?

Two reasons: structural necessity and ownership psychology. On the structural side, high-leverage development demands early liquidity. Pre-selling retail units is the most efficient mechanism to settle construction costs within the four-to-five-year window that most projects operate on. The retail unit is essentially a financing instrument.

On the psychology side, Korean investors have a strong preference for owning a title — a named unit with a land share attached to it. In prime locations like Gangnam, investors will accept rental yields below two percent because the expectation of land value appreciation overrides the operational math. Ownership has a symbolic weight here that income yield alone doesn't fully explain.

Q.Why is vacancy so severe despite the official supply numbers looking stable?

Several things are converging simultaneously. First, the supply that doesn't get counted — retail in KICs, residential podiums, resettlement commercial zones — is substantial and is competing for the same tenant pool as formally designated retail. Second, the macro environment has compressed the survival capacity of small operators: high debt service for landlords, declining footfall for tenants, and a sustained period of weak domestic consumption. Regional and suburban markets outside Seoul's core are bearing the brunt of this.

Third, and this is the structural shift that doesn't reverse, consumers have moved away from convenience-driven shopping. The nearby store at the base of a residential tower used to capture daily spend by default. It no longer does. Destination retail — places with content, atmosphere, and a reason to go — captures that spend now. The convenience-proximity model is broken.

Fourth, investment psychology has effectively shut down. When rental yields can't be justified against borrowing costs, investors stop moving. That illiquidity compounds the vacancy problem and creates real asset devaluation risk across the retail category.

From District Analysis to Building-Level Product Planning

The old analytical framework — studying a commercial district as a single unit, sizing up catchment demographics, projecting traffic — doesn't produce useful answers anymore. The variation in performance within a single district is too large. Two buildings on the same block can have completely different vacancy profiles depending on their internal circulation, their unit configurations, and what decisions were made at the planning stage years ago.

The shift is toward building-level diagnosis: how does a customer move through this specific asset, where are the friction points, which units have structural disadvantages that no tenant can overcome, and what's the realistic range of occupiers that can operate sustainably at this rent?

Category

Macro Approach (Past)

Micro Planning (Present)

Analysis Focus

District traffic and demographics

Internal circulation and unit competitiveness

Core Strategy

Fill by category type

Position by function

Solutions

Rent adjustments to lure tenants

Value-Add strategies for asset re-rating

Q. What are the key diagnostic indicators for a regional retail asset in difficulty?

The first question is always physical: does the building work? Is the circulation logical? Can a customer get from the parking structure to any retail unit without friction? These hardware questions are often the ones that determine whether an asset has any real recovery potential, regardless of what happens with tenants or rents.

The second question is about tenant quality. Filling vacancies with whatever will pay the rent — small real estate offices, phone repair shops, budget nail salons — provides short-term income and destroys long-term asset value. It changes the building's identity in ways that are very hard to reverse. We conduct audits specifically to prevent that.

The third question is about what the landlord can actually execute. A consulting recommendation that requires capital investment the owner doesn't have, or rent-free periods that exceed their debt service capacity, is worthless. The most valuable advice sits at the intersection of what would improve the asset and what is genuinely achievable.

What It Takes to Keep an Asset Alive

A significant share of the distress in the strata retail market is self-inflicted. Developers fragment units to justify higher per-square-meter selling prices, then fill the resulting MD with whoever can pay — regardless of whether those tenants contribute to the building's identity or attract the customers the other tenants need.

The consequence is fragmentation: a building that looks occupied on paper but functions as a collection of disconnected operators rather than a coherent retail environment. Once that pattern is established, breaking it requires either a major capital event or a long vacancy-driven reset.

Q. How do you persuade clients to hold rents when tenants are pushing back hard?

The tenants doing the pushing are well-informed. They know the market rate. Cutting headline rent to fill a unit is a short-term signal that has lasting consequences — it changes what the next tenant expects, and the one after that. We focus instead on the economics of the deal structure: rent-free periods, fit-out contributions, turnover rent arrangements. These tools move the effective economics without moving the face rent, which matters for the asset's valuation.

Q. Why do anchor tenants like Starbucks still matter so much?

Three reasons. First, they establish the building's coordinates. A Starbucks on the ground floor tells every prospective tenant and every prospective buyer what category this asset belongs to. That shorthand is worth real money in leasing and in exit conversations.

Second, anchor tenants with strong corporate covenants improve the asset's financing position. Lenders evaluate retail cash flows through RTI ratios, and a creditworthy anchor sets a floor that improves loan terms for the whole building.

Third, from a disposition standpoint, a Starbucks-anchored building is a fundamentally different conversation with buyers. It de-risks the exit. The buyer knows the anchor doesn't disappear the day they close.

The Fundamentals Haven't Changed

Q. Where do you see real opportunity in the retail investment market right now?

The assets that will come through this period are the ones that were planned around a genuine function — a reason for the building to exist within its community, a catchment it actually serves. The Gwanggyo El Port case is instructive: meticulous MD management, a coherent tenant mix, an operator who understood what the surrounding population needed. That model works.

The blueprint-era is over. The buildings that were sold to investors before they were occupied, on the strength of a location story and a projected yield, are the ones suffering now. The market that comes out of this will be smaller and more rigorous. That's not bad news for investors who can identify real product. It's actually a better environment for those who know what they're looking at.

© Copyright 2026. All rights reserved.

This publication has been prepared in good faith, based on CBRE Korea's current anecdotal and evidence based views of the commercial real estate market. Although CBRE Korea believes its views reflect market conditions on the date of this presentation, they are subject to significant uncertainties and contingencies, many of which are beyond CBRE Korea’s control. In addition, many of CBRE Korea’s views are opinion and/or projections based on CBRE Korea’s subjective analyses of current market circumstances. Other firms may have different opinions, projections and analyses, and actual market conditions in the future may cause CBRE Korea’s current views to later be incorrect. CBRE Korea has no obligation to update its views herein if its opinions, projections, analyses or market circumstances later change.

Nothing in this publication should be construed as an indicator of the future performance of CBRE’s securities or of the performance of any other company’s securities. You should not purchase or sell securities-of CBRE or any other company-based on the views herein. CBRE Korea disclaims all liability for securities purchased or sold based on information herein, and by viewing this publication, you waive all claims against CBRE Korea as well as against CBRE Korea’s affiliates, officers, directors, employees, agents, advisers and representatives arising out of the accuracy, completeness, adequacy or your use of the information herein. No part of this publication may be reproduced, quoted, distributed, or disclosed to any third party without the prior written consent of CBRE Korea.

market

May 26, 2026

2026 Retail Market Insights from the Head of CBRE Korea Retail

From Seoul to the globe, the variable determining the success or failure of retail spaces is shifting from 'where' to 'how'.

market

Apr 13, 2026

It starts with data and is completed in the field

The Essence of the 2026 Retail Market, According to CBRE's Head of Research

market

Apr 13, 2026

Two Years Locked in Permits

The real cost of overseas retail expansion without a project management framework — why permit risk has to be resolved before the lease is signed.

market

Apr 13, 2026

From Supporting Role to Lead: Office Retail

From basement canteen to asset value driver — fifteen years of structural change in Seoul's office building retail, from Centre One to Olive Young N Seongsu.

market

Apr 13, 2026

Why Gut Instinct Kills Your Flagship Store

Thirty-one retail real estate practitioners rank what actually determines flagship store performance.

market

Apr 13, 2026

Know Anyone Good to Set Me Up With?

How leasing decisions are actually made in Seoul's most competitive retail districts — and why the broker in the middle determines the outcome.

market

Apr 13, 2026

New Era, New Areas

Korean brands are going global. The ones that make it understand one thing first: overseas leasing is a credit game, not a rent game.

market

Apr 13, 2026

It's Not That They're Not Spending

Why foreign visitor spending data is replacing card transactions as the next frontier in retail intelligence.

market

Apr 13, 2026

You are so Beauti-cal

Dermatology clinics are now the most sought-after anchor tenants on Gangnam street

market

Apr 13, 2026

Reading a Brand's DNA Before They Do

The retail MD practitioner's job is translation — turning a brand's qualitative language into measurable spatial conditions. What that looks like in practice.