Back

Share

Like

street

Article Highlights

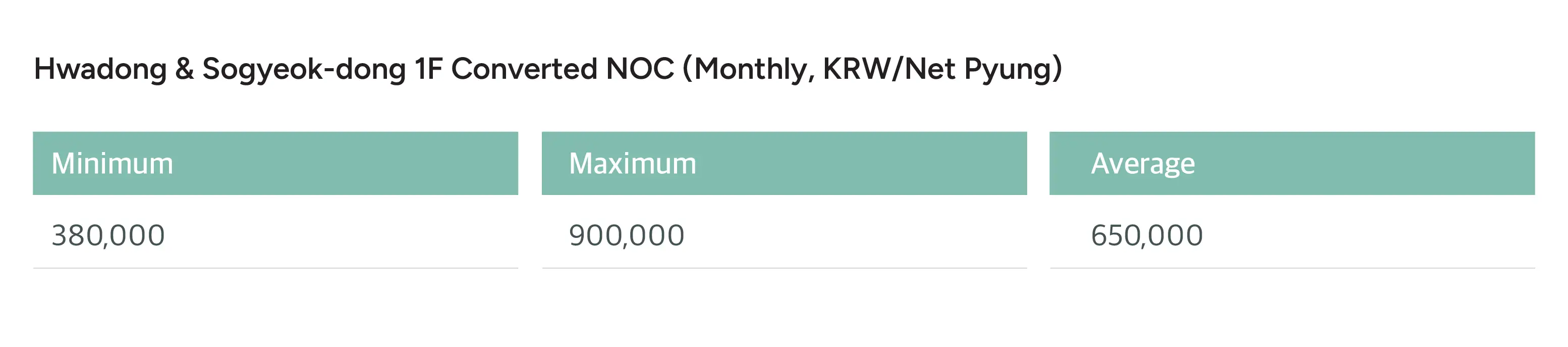

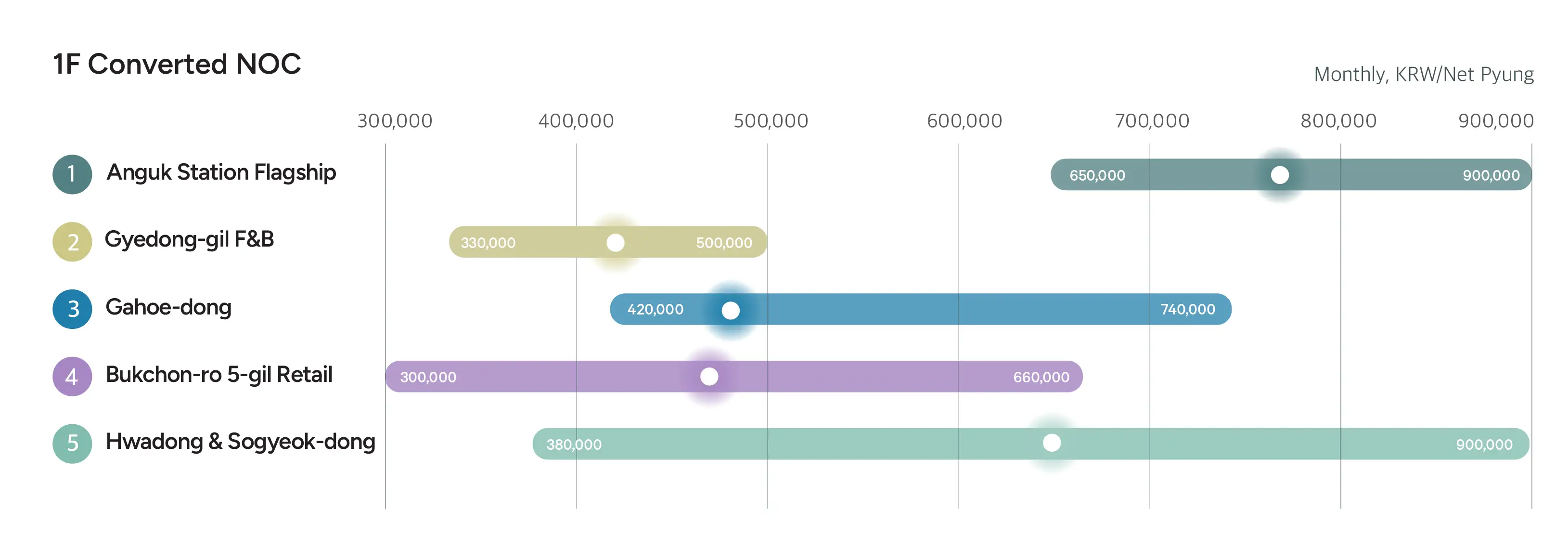

Hwadong and Sogyeokdong form Bukchon's top retail tier for global concept flagships, with whole-building monthly rents of 20–50 million KRW.

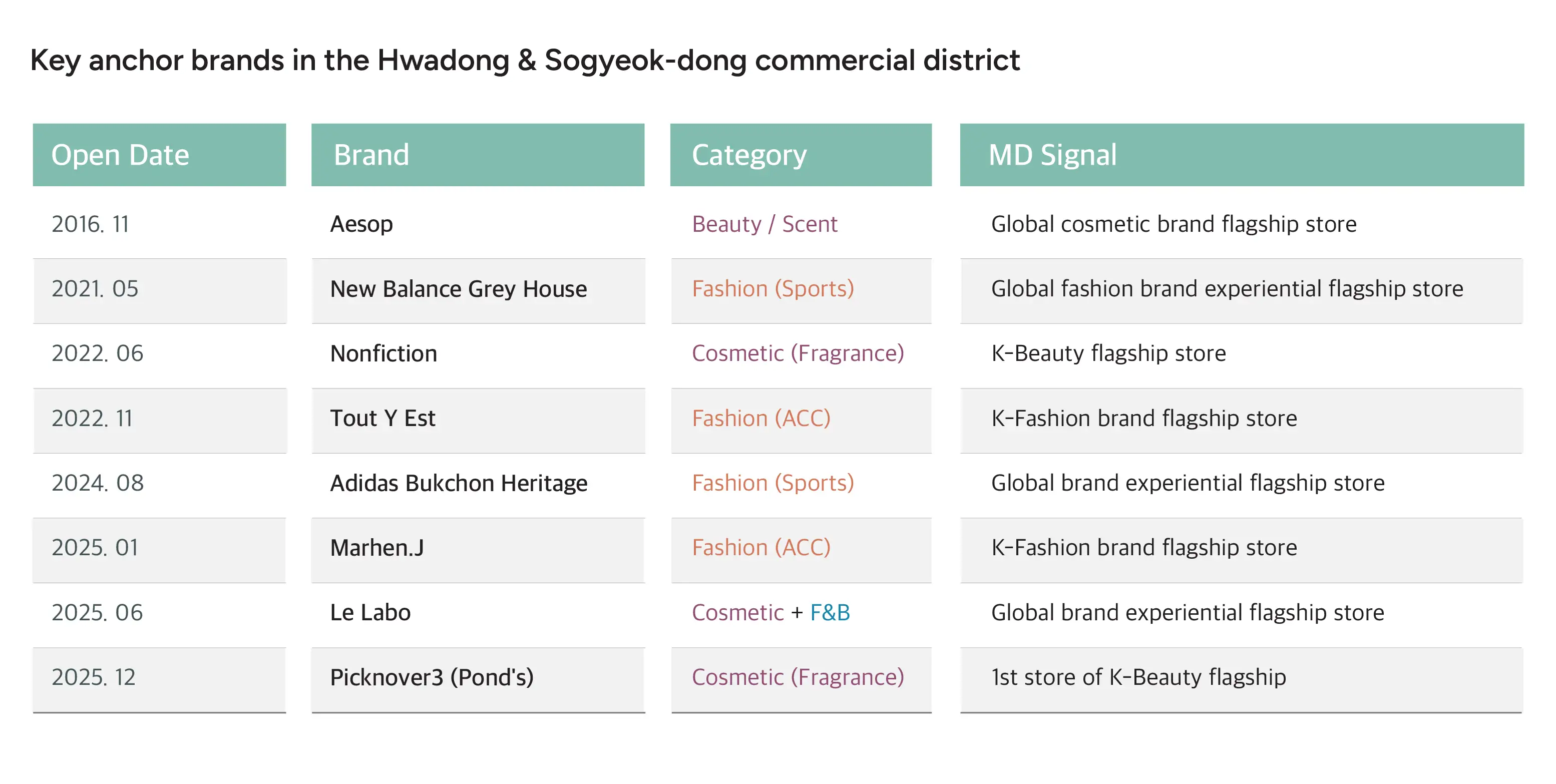

Successive arrivals—Blue Bottle (2019), New Balance (2023), Adidas (2024), and Le Labo (2025)—consistently raise the district's creative bar.

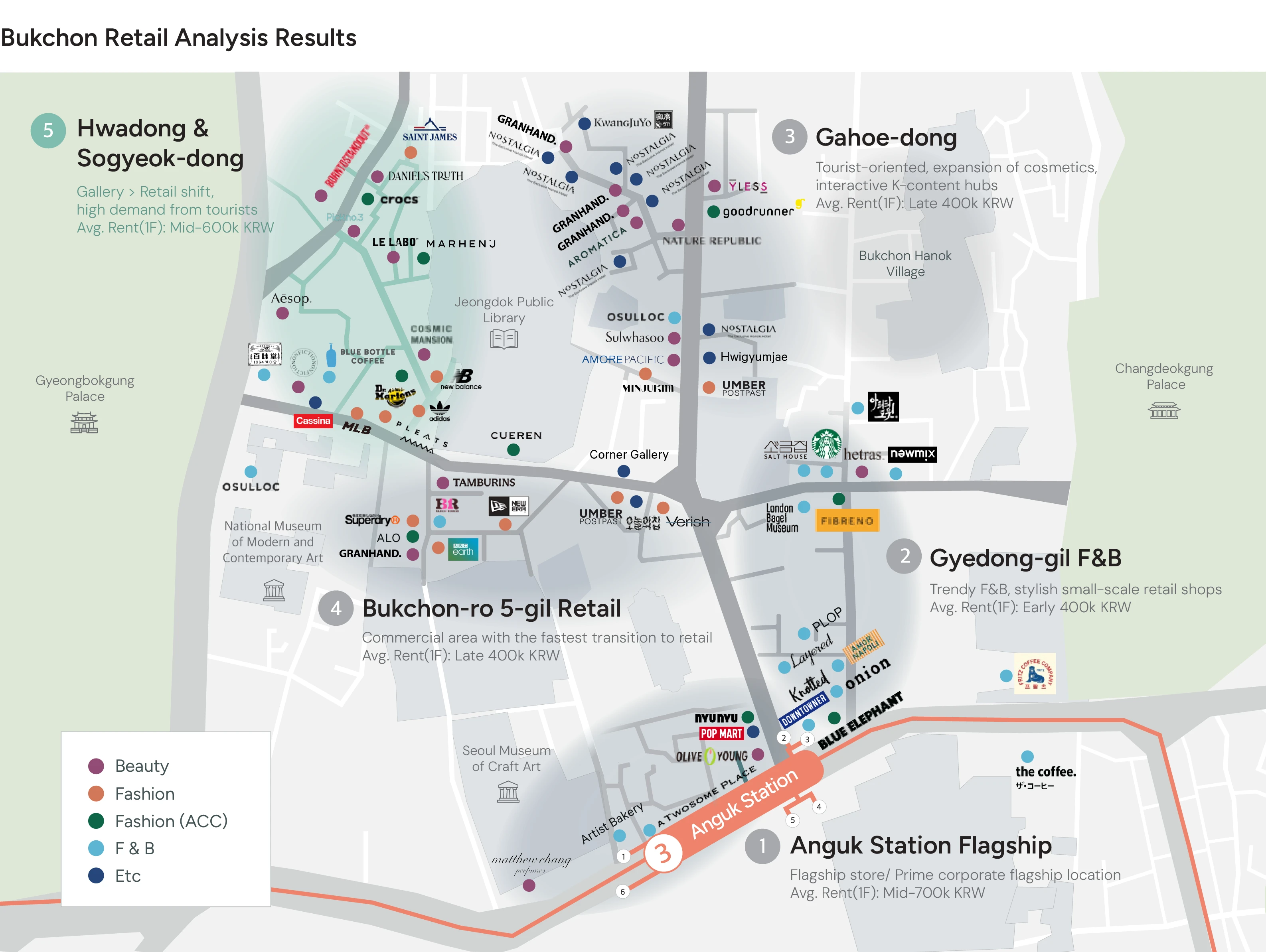

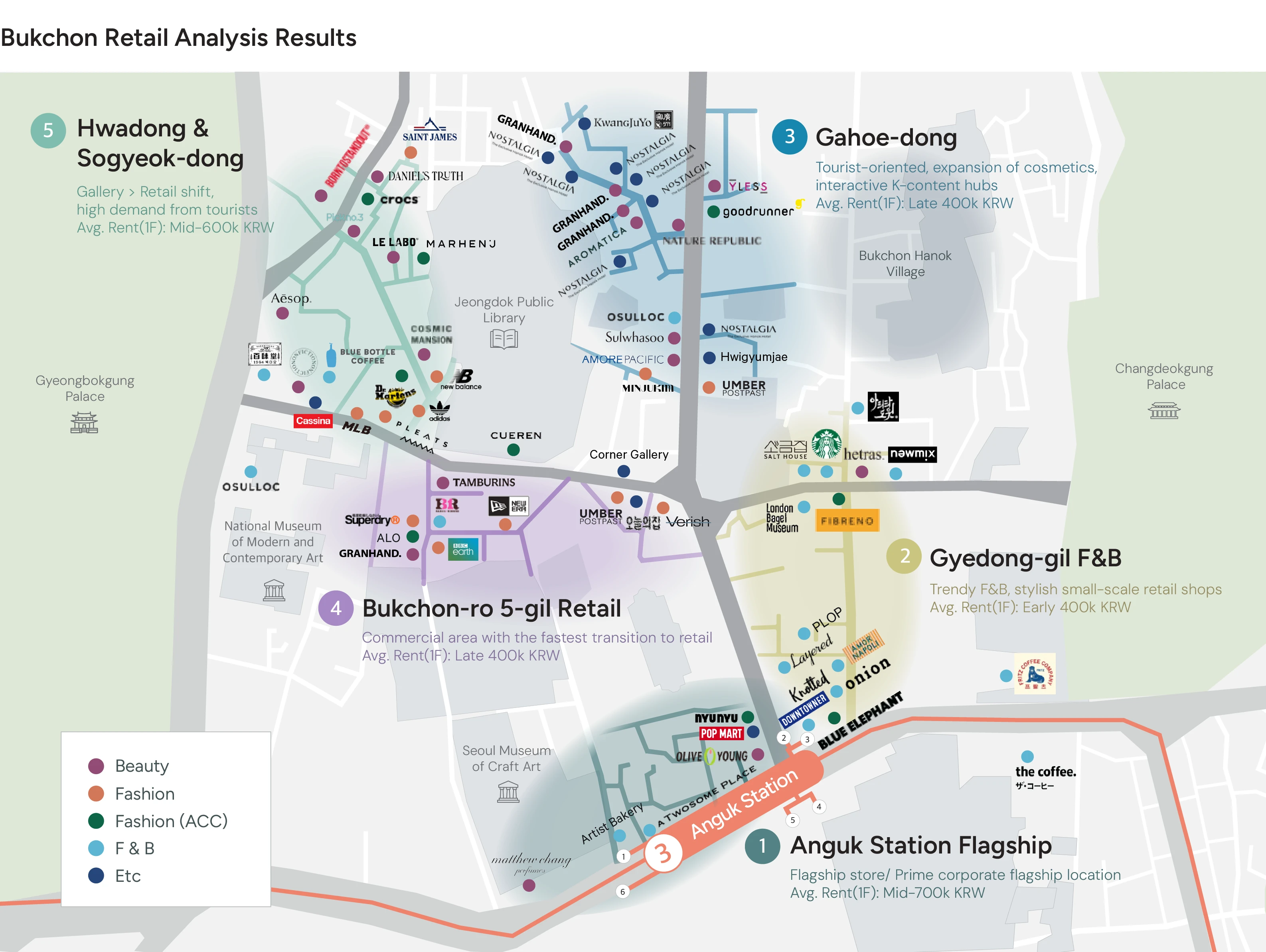

The Bukchon framework is clear: Anguk for scale, Gyedong for F&B, Gahoe for ownership, 5-gil for clustering, and Hwadong/Sogyeokdong for global flagships.

Part 3. Global Mainstream (⑤ Hwadong & Sogyeok-dong)

This section analyzes the strategic occupancy value of the Hwa-dong and Sogyeok-dong core sub-markets, where global powerhouses and high-sensitivity local players converge. In a mature, high-rent environment, we outline the necessity of defining an exclusive brand universe and provide a high-level profitability and feasibility guide for competing alongside global majors.

⑤ Hwa-dong & Sogyeok-dong: The Retail Apex of Bukchon

Formerly the epicenter of the Samcheong-dong district, Hwa-dong and Sogyeok-dong have evolved into Bukchon’s primary landing zone for global retail expansion. The corridor spanning Yulgok-ro 3-gil to Bukchon-ro 5ga-gil has become a high-density cluster of "K-concept" experiential flagships, including Blue Bottle (2019), New Balance (2023), Adidas (2024), and Le Labo (2025).

Strategically positioned along the critical tourist artery connecting Bukchon to Gyeongbokgung Palace, this area functions as a Retail Pinnacle, where global heritage and local "edge" achieve perfect synergy with the adjacent K-retail cluster on Bukchon-ro 5-gil. Currently, market rents for standalone assets rank second only to the Anguk Station hub, with monthly askings stabilized between KRW 20M and 50M.

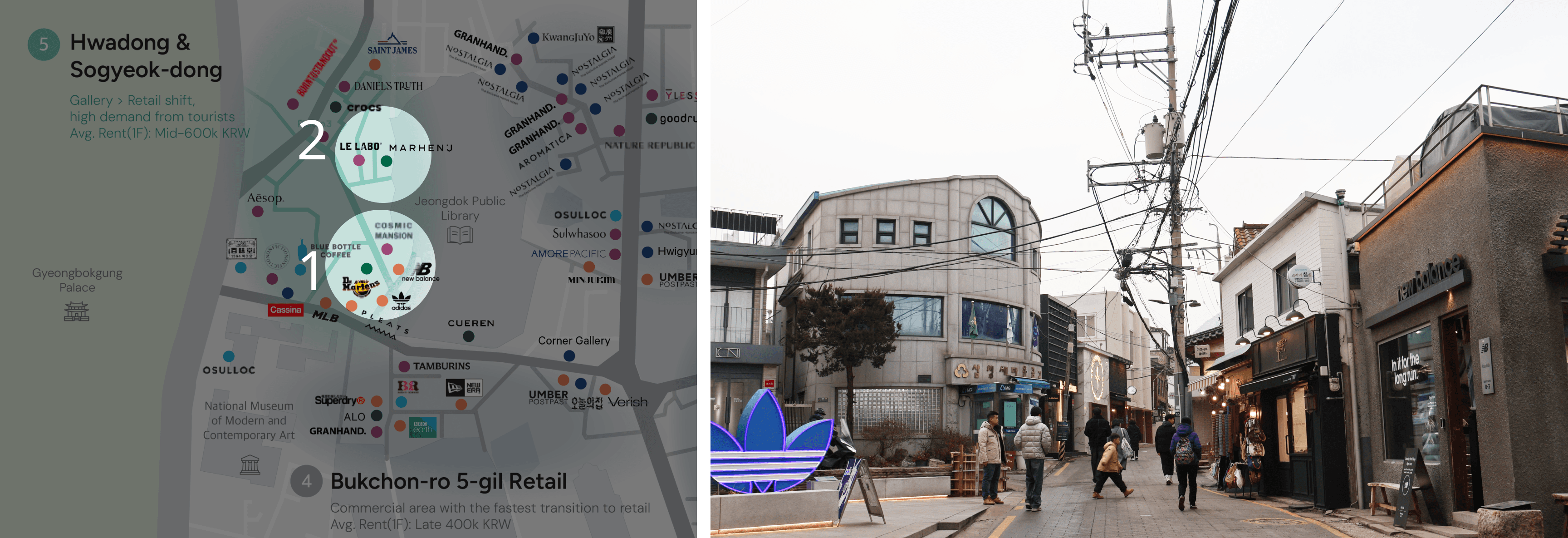

This district serves as the premier battleground for localized flagship reinterpretation. Adidas vs. New Balance: Situated at the entrance of the primary alley, these two giants deploy contrasting spatial experiences—red-brick traditionalism versus concrete modernism—defining the district's unique aesthetic.

Image 1: Fueled by the current "Running Boom," New Balance is seeing a significant uptick in foot traffic, anchoring a high-sensitivity retail geography alongside Cosmic Mansion.

Image 2: Le Labo maximizes Hanok aesthetics to deliver a high-touch, analog brand experience. The continuity into Marhen J exemplifies the district’s unique Retail Mix, where global heritage assets and K-brand agility coexist seamlessly.

This store represents the most organic integration of Bukchon’s regional vernacular with global brand equity. Success here is found in projecting a clear brand identity without Diluting the heritage-heavy atmosphere of the Hanok.

Expert's Insight

In a cluster already saturated with Tier-1 competitors, entry is not about "availability"—it is about Role Definition. Within this tight neighboring landscape, success is dictated by a brand's ability to offer a differentiated mix of Content, Exclusives, and Storytelling. This is a high-barrier-to-entry market reserved for brands capable of converting a premium consumer experience into a sustainable ROI.

Decision Notes

Category | Notes | ||

Pros (Strengths) | Verified destination-based traffic; premium "neighboring" with global anchors ensures high-quality lead generation. High concentration of former gallery assets allows for architecturally distinct flagship directing. | ||

Cons (Weaknesses) | Extremely high barrier to entry due to incumbent dominance; "experiential" content is a mandatory requirement, not an option. Rents have reached a cyclical peak; a rigorous Rent-to-Sales (R/S) ratio and suitability audit is essential. | ||

Target (Recommended Sectors) | Premium Fragrance/Beauty, High-street Fashion, Global Sports Performance, and Major K-brands with high capture rates for international tourists. | ||

Strategic Framework: The 5 Micro-Market Approach

Stop viewing Bukchon as a single district. Strategic success requires a granular focus on five distinct micro-markets.

1. Paradigm Shift: From Sightseeing to Transactional Experiences

Bukchon has transitioned from a passive "scenic" destination to a transactional hub for high-sensitivity categories. It is now a destination where consumers go specifically to "purchase a premium Korean experience." Brands must move beyond the "Showroom" model and treat the space as a revenue-generating content vehicle.

2. Core Decision Metrics by Micro-Zone

Anguk Station (Scale & Speed): A capital-intensive play. High-velocity decision-making is required to compete for dominant footprints against major corporate retailers.

Gyedong-gil (Daily Peak & Turnover): Focus on 7-day stability. The play here is a high-turnover mix of F&B and gift-oriented retail.

Gahoe-dong (Ticket Size & Assetization): The "High-Net-Worth" play. Focus on high average transaction values (ATV). For large-scale footprints, Owner-Occupancy (acquisition) is often more advantageous than leasing for long-term brand equity and asset appreciation.

Bukchon-ro 5-gil (Sensitivity & Neighboring): The K-Brand Cluster. Success requires a "synergy-first" design that leverages the traffic of adjacent K-lifestyle brands.

Hwa-dong & Sogyeok-dong (Content & Universe): The "Global Battleground." Success depends on the brand's "edge"—the ability to defend its exclusive world-view while surrounded by global powerhouses.

3. Operational Risk & Variable Management

Red Zone Constraints (Gahoe-dong): Curfews on tourist entry (17:00–10:00) directly impact labor modeling and Opex. Operational optimization—such as by-appointment-only services or O2O (Online-to-Offline) integration—is required to mitigate these "dead zones."

Total Investment Cost (TIC): Beyond base rent, stakeholders must factor in high key money (premium) in Gyedong/Bukchon-ro 5-gil and significant Hanok-specific Capex (renovation) in Gahoe-dong.

The Necessity of Specialized Advisory: Given the legal complexities, volatile rent spreads, and opaque premium structures in Bukchon, data-driven advisory is non-negotiable. Real estate professionals must provide more than just brokerage; they must deliver a multidimensional analysis of content fit and future terminal value to minimize entry risk and guarantee a successful market position.

Final Take

Success in Bukchon is no longer a function of "Prime Location." It is a function of Micro-Market Alignment. The question is not "Is this a good spot?" but "Does my brand’s DNA align with this specific neighboring?" In this mature market, the spot doesn't make the brand—the positioning does.

© Copyright 2026. All rights reserved.

This publication has been prepared in good faith, based on CBRE Korea's current anecdotal and evidence based views of the commercial real estate market. Although CBRE Korea believes its views reflect market conditions on the date of this presentation, they are subject to significant uncertainties and contingencies, many of which are beyond CBRE Korea’s control. In addition, many of CBRE Korea’s views are opinion and/or projections based on CBRE Korea’s subjective analyses of current market circumstances. Other firms may have different opinions, projections and analyses, and actual market conditions in the future may cause CBRE Korea’s current views to later be incorrect. CBRE Korea has no obligation to update its views herein if its opinions, projections, analyses or market circumstances later change.

Nothing in this publication should be construed as an indicator of the future performance of CBRE’s securities or of the performance of any other company’s securities. You should not purchase or sell securities-of CBRE or any other company-based on the views herein. CBRE Korea disclaims all liability for securities purchased or sold based on information herein, and by viewing this publication, you waive all claims against CBRE Korea as well as against CBRE Korea’s affiliates, officers, directors, employees, agents, advisers and representatives arising out of the accuracy, completeness, adequacy or your use of the information herein. No part of this publication may be reproduced, quoted, distributed, or disclosed to any third party without the prior written consent of CBRE Korea.

Street

Jul 27, 2026

Dosan Park Commercial District Analysis | The Alley Where Brand Drives Land Value

Comparing Seongsu with Dosan: the opposite growth formulas of two Seoul hotspots

street

Jul 13, 2026

Gangnam ② - 75% of Gangnam-daero is Medical

A place where hospitals fill the upper floors emptied by the pandemic, and the wallets of foreigners crowd.

street

Jun 22, 2026

Gangnam ① - Gangnam-daero Retail, Chosen by Global Brands

From 18 vacancies three years ago to just two. The real reason why low-floor retail along Gangnam-daero has made a complete comeback.

street

May 26, 2026

Bangkok Retail 101 ②

Bangkok shopping malls want K-brands. The question is how to get in.

street

May 26, 2026

Bangkok Retail 101 ①

The Developer's Playground: What Sets Bangkok's Retail Evolution Apart from Seoul

street

Apr 13, 2026

Cheongdam: The Art of Elegant Detachment

High jewelry chases the light. Fashion houses build walls. A structural analysis of how capital occupies Cheongdam — and why this street operates by rules that apply nowhere else in Seoul.

street

Apr 13, 2026

Hannam-dong, Seoul's private club. ②

Zero vacancy. Key money reaching 1.3 billion Korean won. Inside Hannam-dong's brand selection market, where who you are matters more than what you offer to pay.

street

Apr 13, 2026

Hannam-dong, a private club in Seoul. ①

Between Seongsu's raw energy and Dosan's polish — how Hannam-dong became Asia's most credible ground for testing a global brand's Korea positioning.

street

Apr 13, 2026

Same Bukchon, Different Strategy ②

Why Amorepacific spent 30 billion won acquiring a hanok compound in Gahoe-dong — and how Bukchon-ro 5-gil became Seoul's fastest-growing K-brand retail cluster.

street

Apr 13, 2026

Same Bukchon, Different Strategy ①

Anguk Station and Gye-dong-gil: The entrance to Bukchon, focusing on the flagship near Anguk Station and the concentration of F&B on Gye-dong-gil.