Back

Share

Like

street

Article Highlights

Zero vacancy in Hannam-dong's primary zone pushes whole-building boulevard key money to 800M–1.3B KRW, repricing the market around brand desirability.

Premium retail entries replacing legacy tenants represent market elevation rather than standard turnover.

Successful Hannam-dong brands lead with space and experience, making the physical store their primary brand argument.

Hannam Series

Part 2: The Price of a Ticket Called Hannam

③ There are no vacancies, only turnover.

④ Key money cases on main roads and back alleys, and competition to preempt locations

⑤ Qualitative changes in foot traffic and redefinition of categories

⑥ Eat, see, and wear.

③ There are no vacancies, only turnover.

The keyword currently cutting through Hannam-dong’s leasing market is not “vacancy.” More precisely, rather than vacancy, it is “movement of occupancy rights (Turnover).” The ground-floor vacancy rate in the main zones now referred to as Hannam-dong’s retail district is effectively converging toward 0%. This is a phenomenon seen only in global high-end retail districts such as Omotesando or Ginza’s main streets in Japan, indicating that a state of “excess demand”—where supply cannot keep up with demand at all—has become entrenched.

This supply-demand imbalance has shifted the center of market indicators from rent to “key money.” Whereas key money in the past was largely about recovering facility investment between self-employed tenants, key money in Hannam-dong today is closer to a “premium claim” for preempting locations. The fact that key money formation has become common not only on main boulevards but also for small back-street units proves that Hannam-dong has already moved beyond a simple rental market into a competitive retail asset market.

Key money no longer remains merely a means for existing tenants to recover their investment. In the actual market, it functions as both a competitive cost for securing a specific location and an indicator of the strategic position a brand seeks within the trade area. In particular, brands planning global flagship stores clearly tend to recognize key money not as a sunk cost, but as “capital expenditure (CAPEX)” for entering high-end commercial districts.

Location preemption cost (Location Premium): A competitive cost willingly paid to occupy a specific address.

Brand Qualification: Proof of having the capital strength and brand power to afford high key money.

Reduction of time cost: Opportunity cost to eliminate the uncertainty of waiting for vacancies and immediately enjoy spillover effects from the district.

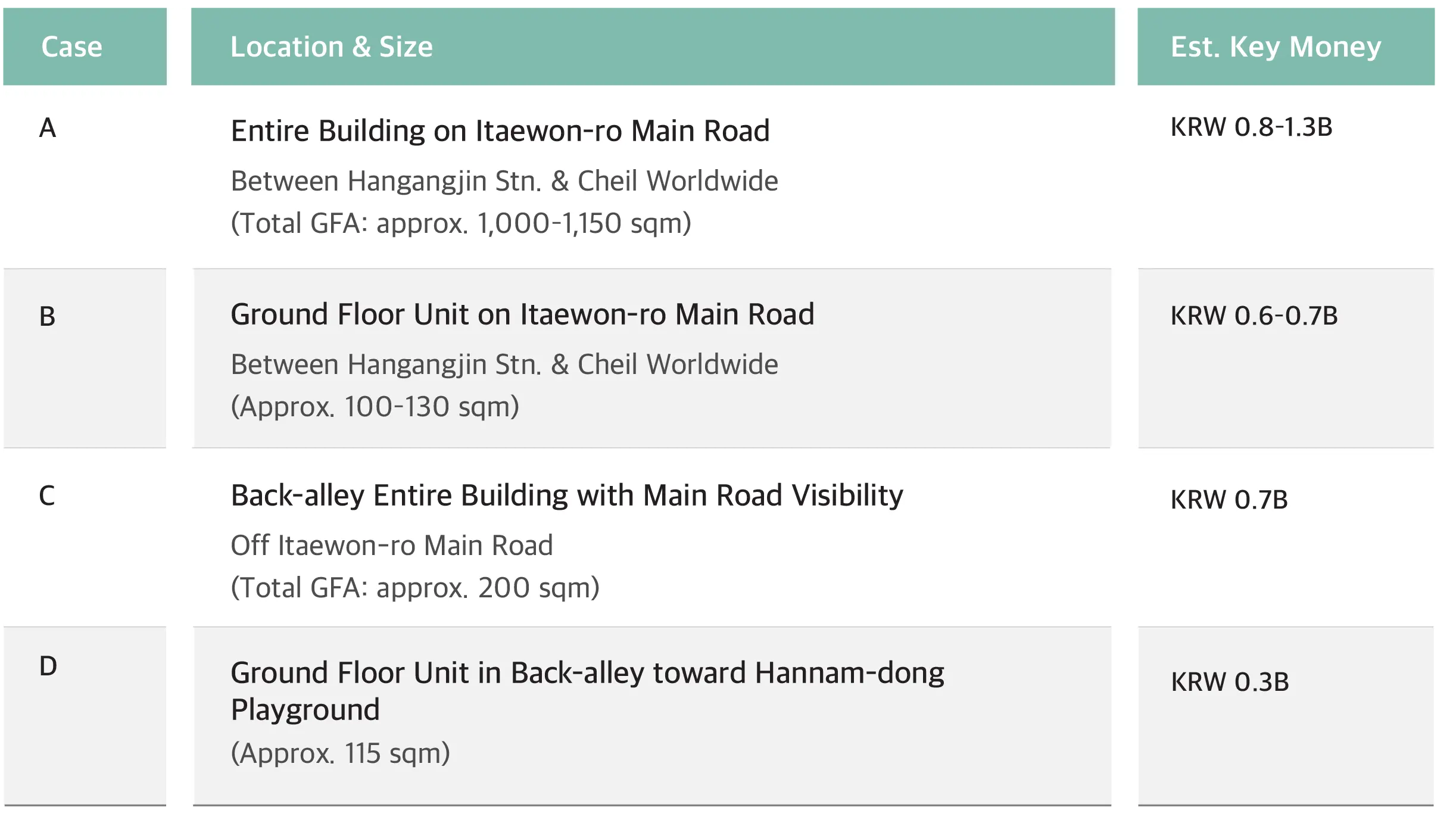

④ On-site key money case examples on main roads and back alleys

For some listings in strategic strongholds, the key money amount itself is a core competitive factor determining whether brand entry is possible. A transaction structure similar to an auction, in the form of pre-bidding, can also arise between landlords and prospective tenants. This shows that key money, beyond being a simple cost, is functioning as the most direct market signal for securing location.

In fact, in major Hannam-dong commercial districts, cases of paying and demanding key money continue to be observed regardless of whether on main roads or back streets, simultaneously reflecting listing scarcity and intensified competition among brands. The very fact that key money is formed means market expectations for the district have risen, while also showing that Hannam-dong is changing from a “rent-centered market” to a “brand-competition-centered market.” In Hannam-dong, key money is no longer just a simple sunk cost; it functions as a strategic investment to preempt scarce locations and as an entry ticket proving a brand’s caliber. In particular, Hannam-dong has recently been evolving beyond a simple F&B-centered consumption area into a massive platform where purpose-driven, high-involvement consumers and foreign tourists mix. This qualitative change in foot traffic signals a fundamental reset of tenant composition and leads to the next discussion on how Hannam-dong is redefining Seoul’s retail map.

Expert's Insight

“As you can see from the key money case status in Hannam-dong presented above, Hannam-dong today is a trade area where, more than ‘how much can you pay,’ ‘who comes in’ matters more, and the formation and expansion of key money can be said to be the most direct market signal of this structural change. In Hannam-dong, key money currently plays a role as a kind of admission fee. For example, when a certain overseas contemporary brand recently entered a back alley, the key money it paid to the existing tenant was effectively a premium on the location’s ‘scarcity’. A 0% ground-floor vacancy rate in Hannam-dong means there’s no space even if you have money. The reason brands offer key money first to secure a spot is that the moment they plant their flag in Hannam-dong, Hannam-dong’s scarcity gives the brand tangible marketing effects.”

⑤ Qualitative changes in foot traffic and redefinition of categories

The key factor explaining Hannam-dong is the qualitative change in floating population. While simple pass-through traffic has decreased, visit-and-stay traffic with specific purposes has clearly increased. A consumption path has taken root in which people link flagship stores with cafes, exhibitions, and select shops. In particular, the daytime weekday foreign visitor share comes not for Myeong-dong-style shopping, but to experience K-fashion and Seoul’s distinctive lifestyle—that is, ‘local hipness.’ Domestic visitors are mainly a high-sensitivity consumer group in their 20s to 40s, consuming Hannam-dong as the ‘next stage after Seongsu.’ Although Chinese tourists make up an overwhelming share of foreigners visiting areas near Hannam-dong, visits by Japanese and Southeast Asian tourists, as well as independent travelers from Europe and the Americas, are also steadily increasing.

⑥ Eat, see, and wear.

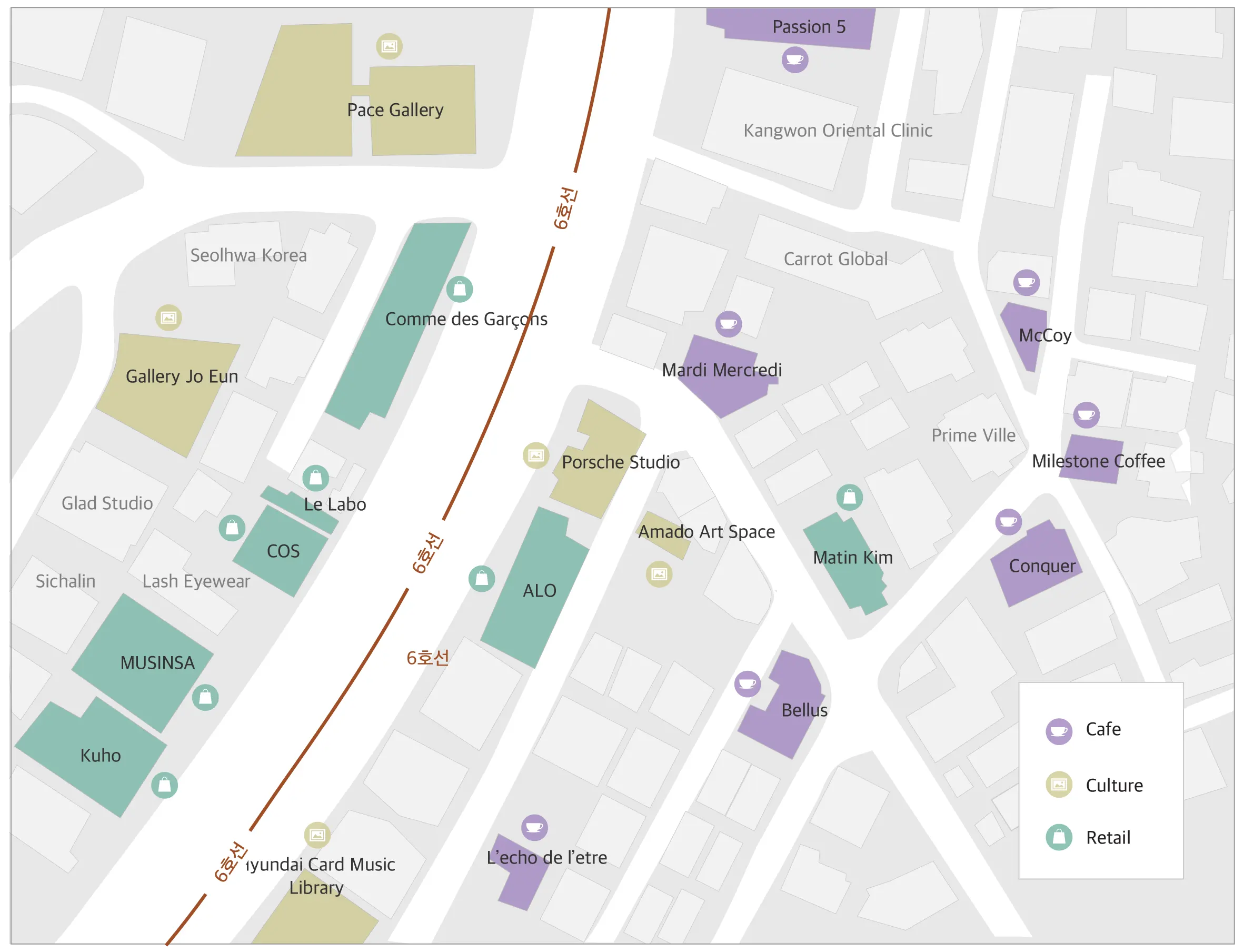

Domestic visitors are fashion- and lifestyle-savvy consumers in their 20s to 40s, showing a pattern of consuming Hannam-dong as the “next stage after Seongsu,” while foreign visitors come to experience K-fashion and K-lifestyle, consuming purchasing, photos, and experiences all at once. Hannam-dong’s real strength, as seen on the map, is that the domains of eating, seeing, and wearing are tightly interwoven.

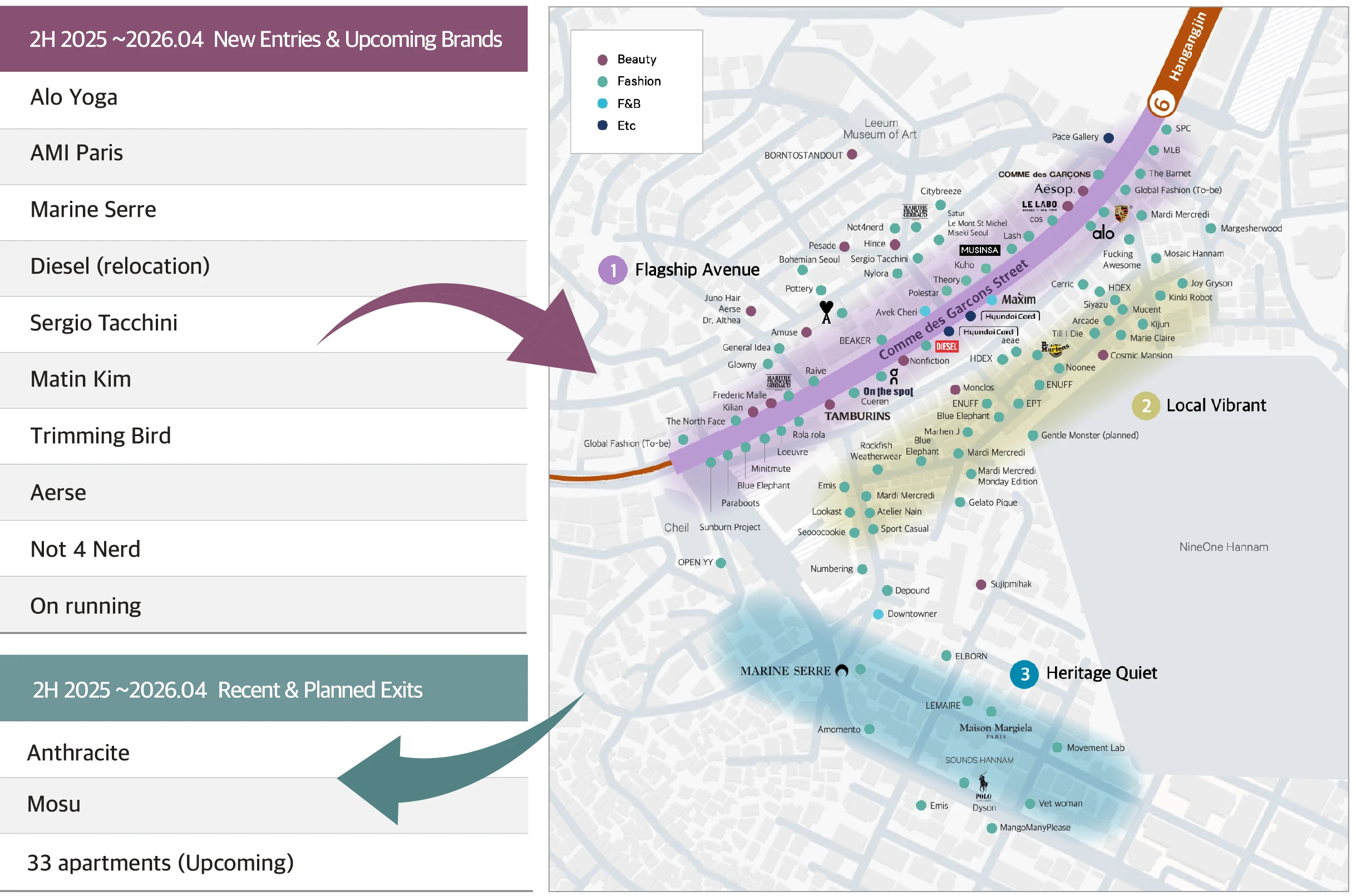

The direction of Hannam-dong shown by In & Out brands

Recently, tenant turnover (In & Out) in Hannam-dong does not simply mean the end and start of lease contracts; it means a reset of the commercial district. The common traits of incoming brands are clear. They prioritize spatial experience over sales and brand message over product. In particular, the replacement of existing F&B units with global fashion and hybrid lifestyle brands shows that Hannam-dong has upgraded from a “food-and-drink alley” to a “hub of brand worldviews.”

In (Incoming): Alo Yoga, AMI Paris, Marine Serre, Diesel (relocation), Sergio Tacchini, Matin Kim, Trimming Bird, Aerse, Not 4 Nerd, On running, etc. Global contemporary and rising local brands are mixing to increase the district’s density.

Out (Exiting): Anthracite, Mosu, Kasina, 33 apartments (planned), etc. The departure of some symbolic brands is not a decline of the district, but closer to selective evolution occurring in the process of being replaced by brands with greater capital power and clearer concepts.

The meaning of Hannam-dong: Where Seoul’s sensibility receives final approval

Even the scene at the lease negotiation table is changing. In the past, the key questions were how much could be sold and whether a tenant had the stamina to pay monthly rent, but Hannam-dong is different now. How powerful the brand is, how clear the concept is, and whether there is visible potential for global expansion are the real criteria that move landlords.

The category mix is also becoming more advanced. If it used to be just clothing stores and cafes, now it has evolved into a complex ecosystem mixing global contemporary fashion, art, cultural content, beauty, and lifestyle experimental stores. For domestic brands, it is a proving ground to stand shoulder-to-shoulder with global giants and prove their caliber; for overseas brands, it is a powerful first impression cast into the Asian market.

In this flow, Hannam-dong does not bother comparing itself with Seongsu or Myeong-dong. Rather than competing with them, it simply holds its own place as a stage marking the peak of Seoul’s retail ecosystem. Hannam-dong’s unique mood—exotic yet refined in a deeply Korean way—will remain an unparalleled cluster where high-end brands want to plant their flag first.

Hannam-dong is a unique zone where global trends and local sentiment are filtered with the greatest density. As we enter an era where opening in the district itself becomes a brand insignia, the battle among global fashion and lifestyle brands to enter is expected to become even fiercer.

© Copyright 2026. All rights reserved.

This publication has been prepared in good faith, based on CBRE Korea's current anecdotal and evidence based views of the commercial real estate market. Although CBRE Korea believes its views reflect market conditions on the date of this presentation, they are subject to significant uncertainties and contingencies, many of which are beyond CBRE Korea’s control. In addition, many of CBRE Korea’s views are opinion and/or projections based on CBRE Korea’s subjective analyses of current market circumstances. Other firms may have different opinions, projections and analyses, and actual market conditions in the future may cause CBRE Korea’s current views to later be incorrect. CBRE Korea has no obligation to update its views herein if its opinions, projections, analyses or market circumstances later change.

Nothing in this publication should be construed as an indicator of the future performance of CBRE’s securities or of the performance of any other company’s securities. You should not purchase or sell securities-of CBRE or any other company-based on the views herein. CBRE Korea disclaims all liability for securities purchased or sold based on information herein, and by viewing this publication, you waive all claims against CBRE Korea as well as against CBRE Korea’s affiliates, officers, directors, employees, agents, advisers and representatives arising out of the accuracy, completeness, adequacy or your use of the information herein. No part of this publication may be reproduced, quoted, distributed, or disclosed to any third party without the prior written consent of CBRE Korea.

Street

Jul 27, 2026

Dosan Park Commercial District Analysis | The Alley Where Brand Drives Land Value

Comparing Seongsu with Dosan: the opposite growth formulas of two Seoul hotspots

street

Jul 13, 2026

Gangnam ② - 75% of Gangnam-daero is Medical

A place where hospitals fill the upper floors emptied by the pandemic, and the wallets of foreigners crowd.

street

Jun 22, 2026

Gangnam ① - Gangnam-daero Retail, Chosen by Global Brands

From 18 vacancies three years ago to just two. The real reason why low-floor retail along Gangnam-daero has made a complete comeback.

street

May 26, 2026

Bangkok Retail 101 ②

Bangkok shopping malls want K-brands. The question is how to get in.

street

May 26, 2026

Bangkok Retail 101 ①

The Developer's Playground: What Sets Bangkok's Retail Evolution Apart from Seoul

street

Apr 13, 2026

Cheongdam: The Art of Elegant Detachment

High jewelry chases the light. Fashion houses build walls. A structural analysis of how capital occupies Cheongdam — and why this street operates by rules that apply nowhere else in Seoul.

street

Apr 13, 2026

Hannam-dong, a private club in Seoul. ①

Between Seongsu's raw energy and Dosan's polish — how Hannam-dong became Asia's most credible ground for testing a global brand's Korea positioning.

street

Apr 13, 2026

Same Bukchon, Different Strategy ③

Blue Bottle, New Balance, Adidas, Le Labo — how Hwadong and Sogyeokdong became the global flagship core of Seoul's Bukchon retail market.

street

Apr 13, 2026

Same Bukchon, Different Strategy ②

Why Amorepacific spent 30 billion won acquiring a hanok compound in Gahoe-dong — and how Bukchon-ro 5-gil became Seoul's fastest-growing K-brand retail cluster.

street

Apr 13, 2026

Same Bukchon, Different Strategy ①

Anguk Station and Gye-dong-gil: The entrance to Bukchon, focusing on the flagship near Anguk Station and the concentration of F&B on Gye-dong-gil.